- Previous Article

India’s financial sector has faced many challenges in recent decades, with a large, negative, and persistent credit to GDP gap since 2012. We examine how cyclical financial conditions affect GDP growth using a growth-at-risk (GaR) approach and analyze the link between bank balance sheets, credit growth, and long-term growth using bank-level panel regressions for both public and private banks. We find that on a cyclical basis, a negative shock to credit or a rise in macro vulnerability all shift the distribution of growth to the left, with lower expected growth and higher negative tail risks; over the long term, the results indicate that higher credit growth, arising from better capitalized banks with lower NPLs, is associated with higher GDP growth.

- I. Introduction

India’s financial sector has faced many challenges in recent decades, including a rapid increase in non-performing assets (referred hereafter as non-performing loans, NPLs)after the global financial crisis (GFC) and the 2018–2019 run on non-banking financial companies (NBFCs). Credit growth has been weak for sometime, with a large, negative, and persistent credit to GDP gap since 2012. Just as the balance sheets of the financial sector started to gradually improve, the COVID-19 shock hit the economy, raising concerns about a new wave of NPLs and corporate defaults. At the same time, real GDP growth averaged 6.7 percent from 2011 to 2018, before moderating to 3.7 percent in 2019 (NBFC crisis) prior to the COVID-19 crisis. As India recovers from the pandemic, strong GDP growth will need to be sustained over the near- and medium-term for India to achieve many of its development goals.

This paper examines the nexus between the financial sector in India and economic growth and analyzes the potential impact of financial sector weakness on India’s economic growth. The financial sector could affect economic growth through multiple channels, with both cyclical and long-term effects. This paper focuses on these two channels and abstracts from the question of whether the size or structure of the financial system is important for growth. 2 Specifically, this paper first examines how cyclical financial conditions affect GDP growth using a growth-at-risk (GaR) approach ( Adrian et al., 2019 ) and assesses how financial conditions and credit risks could be associated with expected GDP growth going forward. Second, the paper analyzes the relationship between bank balance sheets, credit growth, and long-term growth using bank-level panel regressions for both public and private banks accounting for about 85 percent of total banking sector assets.

This paper is related to two strands of literature on financial sector and economic growth. The first strand examines the cyclical perspective. Adrian et al. (2019 ), Prasad et al. (2019 ) and IMF (2017) apply the GaR approach to use the information content of financial indicators to forecast risks to growth. Both fast-moving asset prices and slow-moving credit aggregates are found to be useful predictors of future output growth. For example, Ang, Piazzesi, and Wei (2006) highlight the importance of the yield curve, particularly short rate, in predicting GDP growth. Goodhart and Hofmann (2008) assess the linkages between credit, money, house prices, and economic activity in 17 industrialized countries over the last three decades and find that shocks to credit have significant repercussions on economic activity. Furthermore, recessions associated with financial crises are shown to have more severe and prolonged impact on the economy than typical recessions (see, for example, Claessens, Kose, and Terrones 2011a , 2011b ). The second strand of the literature examines the link between the health of the banking sector and real GDP growth. For example, Levine (2005) found that countries with large, privately owned banks tend to channel credit to private enterprises and liquid stock exchanges and experience faster economic growth. Using balance sheet data for international banks from a range of advanced economies, Gambacorta and Shin (2016) and Muduli and Behera (2021) show that well-capitalized banks enjoy lower costs of debt financing compared to more leveraged competitors, which in turn translates into higher annual credit growth and can impact monetary policy transmission.

The GaR analysis finds that higher credit and lower NPLs are associated with higher GDP growth in the near- and medium-term. More favorable credit conditions are particularly important during periods with low growth. A negative shock to credit and leverage could shift the entire growth distribution to the left, with lower expected growth and higher negative tail risks. The results for the second section of the paper confirm that in India, at least for private banks, the level of capitalization is strongly correlated with credit growth. The relationship for public banks appears to be much weaker. Additionally, it is when those banks which are better capitalized extend more credit that India observes higher real GDP growth, but only on the condition that these banks do not have excessive NPLs.

The paper is organized as follows. Section II examines the link between cyclical financial conditions and growth. Section III analyzes the link between financial sector and long-term growth. Section IV offers some concluding remarks.

II. Cyclical Financial Conditions and Near-Term Growth

- A. Data and Stylized Facts

A quarterly database is constructed for macro-financial data for India from 2000Q1 to 2021Q3. The database covers key macro-financial variables, including GDP growth, inflation, policy rate, bond yields, sovereign spreads, stock prices, credit growth, credit to GDP gap, the NPL ratio, world growth, oil prices and exchange rates, and other macroeconomic variables. The database draws from multiple sources, including Haver Analytics, Reserve Bank of India, Central Statistics Office, International Monetary Fund, Bank of International Settlements, Ministry of Statistics and Programme Implementation, Bombay Stock Exchange, Energy Information administration/Chicago Mercantile Exchange, and Bloomberg. The detailed definition of the underlying data and sources can be found in Annex Table 1 .

The analysis focuses on the broad definition of credit that covers both bank credit and debt securities. The credit-to-GDP ratio peaked at around 106 percent in 2012 and declined to around 90 percent in 2021, while the bank-credit-to-GDP ratios currently stands at around 55 percent. Following a period of double-digit credit growth, the credit-to-GDP gap 3 turned negative from 2012 ( Figure 1 ). The decline in credit since 2012 was mostly driven by the deleveraging process of the corporate sector. Corporate credit growth slowed from a peak of close to 30 percent in 2008 to zero at its trough, with a sharper decline in corporate credit growth compared with the household segment. At the same time, the broad credit growth also experienced a sharper slowdown than bank credit growth, suggesting that the deleveraging process not only took place in the banking sector, but also in broader debt financing. The NPL ratio peaked at around 11 percent in 2017 but has since come down to around 8 percent.

Credit and Leverage

Citation: IMF Working Papers 2022, 137; 10.5089/9798400216404.001.A001

- Download Figure

- Download figure as PowerPoint slide

- B. Methodology

The GaR analysis in the India economy follows closely the approach of Adrian et al. (2019 ) and Prasad et al. (2019 ). GaR provides a tractable and robust estimation of the severity and the likelihood of a sharp economic slowdown. The model uses information contained in financial prices and aggregates to identify macro-financial linkages and gauge financial vulnerabilities. Importantly, GaR captures the entire growth distribution at different future horizons—reflecting both downside and upside risks—in addition to central-scenario growth forecasts. The concept helps better understanding of the relative importance of key drivers of future growth.

The first step of GaR analysis involves aggregating the set of macrofinancial variables into economically meaningful groups (“partitions”). In this approach, five main partitions of macrofinancial variables are considered ( Table 1 ): 1) domestic prices, which capture the policy interest rate, 10 -year treasury bond yield, sovereign bond spread, and a change in stock prices; 2) credit and leverage, which includes credit growth, the credit to GDP ratio, the credit to GDP gap, and the NPL ratio; 3) macroeconomic vulnerabilities, which capture inflation, the current account balance to GDP ratio, and the short-term external debt to reserve ratio; 4) external prices, which include changes in oil prices and exchange rates; and finally 5) external macro that captures world GDP growth. These partitions are then computed using the principal component analysis (PCA) that aggregates information about common trends among these macro-financial variables.

Partition of Macro-Financial Variables

| Domestic prices | Credit and leverage | Macro vulnerabilities | External prices | External Macro |

|---|---|---|---|---|

The second step of GaR uses a quantile regression approach to estimate the impact of financial conditions on different quantiles of real GDP growth in India. The following specification of the quantile regression is estimated:

where y t + h q captures the h quarter ahead GDP growth (year-on-year) for quantile q; X 1,t denotes the partition for domestic prices; X 2,t captures the partition of credit and leverage; X 3,t denotes the partition of macroeconomic vulnerabilities; X 4,t represents the partition of external prices; and X 5,t captures the partition of external macro conditions. Furthermore, ε t + h q denotes the residual, and α q , β 1 q , β 2 q a n d β 3 q are the coefficients of the regression. In the analysis, five different quantiles (or percentiles) are considered, at 10 percent, 25 percent, 50 percent, 75 percent, and 90 percent, which capture the linkages between macro-financial conditions and growth at different points of the future growth distribution. For example, the 10 percent quantile captures low growth periods (when growth rate is at the bottom 10 percentile), while the 90 percent quantile features high growth periods. Multiple forecast horizons (for example, 4 quarter ahead to 16 quarter ahead) are also considered to examine the impact of financial conditions on near-and medium-term growth.

Based on the results of the quantile regression, a t-skew distribution is then used to derive the probability density distribution of future GDP growth. The GaR framework could also be used to conduct scenario analysis, which examines the impact of shocks to the different partitions including credit and leverage, domestic prices, and macroeconomic vulnerabilities on the future growth distribution.

Macro-financial Partitions and Loadings

The relationship between different macro-financial partitions and real GDP growth in India is examined. As seen in Figure 2 , the credit to GDP ratio, the credit to GDP gap and credit growth have positive loadings on the first principal component 4 of credit and leverage indicators, while the NPL ratio has a negative loading. Therefore, an increase in the credit and leverage summary indicator would imply higher credit or more favorable credit conditions. After peaking in 2005/2006, the credit and leverage indicator has been on a downward trend since 2011/2012, coinciding with the period of negative credit to GDP gap.

Macro-Financial Partitions and Loadings

On domestic prices, 10-year treasury bill yields, policy interest rate and sovereign yields have a positive sign in the principal component, while a change in stock prices has a negative loading. An increase in the principal component of domestic prices would then imply a tightening in price-based financial conditions. In the first half of the sample, there was an inverse relationship between real GDP growth and the summary domestic price indicator, where a tightening in the price-based financial conditions is associated with a decline in growth. More recently, there has been a continued loosening of financial conditions, with the link between price-based financial conditions and economic growth less pronounced.

On macro economic vulnerabilities, short term external debt and inflation have positive loadings on the principal component, while the current account balance has a negative sign. A rise in the principal component of macroeconomic vulnerabilities would then imply higher vulnerabilities in the economy. Figure 2 shows that macroeconomic vulnerabilities peaked in 2012/13 but has been on a downward trend since then.

Scenario Analysis

A scenario analysis is conducted and considers a two standard deviation negative shock to the credit and leverage partition ( Figure 3 ). A decline in the credit and leverage partition (here, referring to the principal component) would imply a tightening of the credit conditions and a worsening in credit quality, as measured by the NPL ratio. The blue line captures the density before shock and the red line captures the one afterwards. Following the negative shock, the entire distribution of GDP growth would shift to the left. The mode of the 4 quarter ahead GDP growth would decline from 7.6 percent to 5.3 percent. Moreover, the tail risks would increase considerably, with the 5 percent GaR shifting from -5.7 percent to -12.2 percent. In other words, there was a 5 percent probability that growth could be below-5.7 percent prior to the shock. However, after the shock, there is 5 percent probability that growth could be below-12.2 percent, and the probability of growth below -5.7 percent increased to 11 percent, a much more severe tail outcome.

Growth-at-Risk: Shock to Credit and Leverage

In addition, a two standard deviation positive shock to the domestic prices partition and to the macro vulnerability partition are considered, respectively. An increase in the domestic prices partition would imply a tightening in the price-based financial conditions ( Figure 4 , left chart). The mode of the 4 quarter ahead GDP growth would decline from 7.6 percent to 7 percent, with a slight shift of the growth distribution to the left following the shock. The relatively milder impact of the domestic price shock could be potentially attributed to be weaker relationship between domestic prices and growth in recent years. On macroeconomic vulnerabilities ( Figure 4 , right chart), a two-standard deviation positive shock (higher vulnerabilities) would imply a decline in 4 quarter ahead GDP growth from 7.6 percent to 5.9 percent (mode), with the growth distribution shifted to the left, capturing higher tail risks.

Growth-at-Risk: Shocks to Domestic Prices and Macroeconomic Vulnerabilities

Term Structure of Credit and Leverage Indicators

Furthermore, the term structure of the credit and leverage indicators and the impact on GDP growth across different horizons is examined. Specifically, the 4 quarter, 8 quarter, 12 quarter and 16 quarter ahead quantile regression results are considered. In Figure 5 , the y-axis refers to the coefficient of the credit and leverage partition in the quantile regression (Equation (1)) and the x-axis refers to the different quantiles, capturing GDP growth at the 10 th , 25 th , 50 th , 75 th and 90 th percentiles. The results suggest that high credit and low NPLs have a positive and significant impact on GDP growth across all horizons. Furthermore, the impact is even larger at lower quantiles when GDP growth is lower. In other words, a favorable credit condition with higher credit and stronger credit quality is particularly important in supporting the economic recovery during periods of low growth.

Growth-at-Risk: Term Structure for Credit Indicators

As a robustness check, we also consider an alternative specification focusing on the bank credit to GDP ratio and bank credit growth, instead of the broader concept of credit. The results are found to be robust. A negative shock to the credit and leverage partition would again shift the GDP growth distribution to the left. Higher bank credit and stronger credit quality are particularly supportive to the economy when growth is relatively weak (see Annex Figures 1 and 2 ).

Investment- and Consumption-at-Risk

Having established the importance of credit and leverage variables for GDP growth, we also examine the extent to which they influence components of GDP growth, such as investment and consumption. Inequation (1), we consider y t + h q as the h quarter ahead investment and consumption growth (year-on-year) for quantile q , respectively.

Similar to the aggregate GDP growth, we consider the impact of a two standard deviation negative shock to the credit and leverage partition ( Figure 6 ) on investment and consumption. Following the negative shock, both the distributions of investment and consumption growth would shift to the left. The mode of the 4 quarter ahead investment growth would decline from 20 percent to 10.4 percent, with the 5 percent Investment-at-Risk shifting from-10.9 percent to -19.2 percent. In other words, there was a 5 percent probability that investment growth could be below-10.9 percent prior to the shock. However, after the shock, there is 5 percent probability that growth could be below-19.2 percent, a much more severe tail outcome. For consumption, the mode of the 4 quarter ahead consumption growth would decline from 12.5 percent to 6.7 percent, with the 5 percent Consumption-at-Risk shifting from -5 percent to -15.6 percent, also implying higher tail risks.

Investment-at-Risk and Consumption at Risk: Shock to Credit and Leverage

- D. Policy Discussions

The results from GaR suggest that higher credit and lower NPLs are associated with higher GDP growth in the near- and medium-term. A negative shock to credit and leverage (lower credit and higher NPL ratio) could shift the distribution of GDP, investment, and consumption growth to the left, with lower expected growth and larger downside risks.

During periods of low economic growth, policies to support credit growth and to strengthen balance sheets would be particularly important. In this regard, policy responses such as credit guarantee schemes for MSMEs, loan restructuring scheme for COVID-affected borrowers were important to support credit growth and cushion the economic impact of the pandemic.

Going forward, further efforts to make support measures even more targeted and facilitate the exit of non-viable firms may be warranted. In addition, financial regulators should continue to ensure that loans benefiting from COVID-related restructuring schemes are closely monitored and properly provisioned for, to safeguard the health of financial sector balance sheets and help support the economic recovery.

III. Financial Sector and Long-Term Growth

Several studies document that poor capitalization and weak asset quality negatively impact banks’ ability to provide credit to the economy. Using balance sheet data for international banks from a range of advanced economies, Gambacorta and Shin (2018) show that well-capitalized banks enjoy lower costs of debt financing compared to more leveraged competitors, which in turn translates into higher annual credit growth. Muduli and Behera (2021) find similar evidence in India, of a positive correlation between bank equity and credit growth, and that this plays a role in monetary policy transmission. Blattneret al. (2019) look at a macro-angle and show that less-capitalized banks cut lending in response to higher capital requirements, which potentially contribute to weaker productivity growth. This section of the paper builds on this literature by examining the role of balance sheets of Indian banks on credit growth, and ultimately overall output growth in the economy. The focus is, in particular, on the differential role of public and private banks in driving credit growth.

Data for the main bank-level variables of interest (cost of funding, growth of debt funding, credit growth, and bank capitalization) as well as bank-level control variables (non-performing assets, return on assets) are from FitchConnect. The sample is at an annual frequency from 1998–2021. Only public banks and private banks are kept in the sample, excluding such entities as non-bank financial companies, foreign banks and development banks. 5 The sample accounts for about 85 percent of total assets in the Indian financial sector in any given year of the sample. For the macro-level analysis, the data on GDP growth and various India-level or global controls are from the Reserve Bank of India via Haver and CEIC. Details of the data and sources are available in Annex Table 2 .

The main explanatory variable is bank-level capitalization which, based on existing literature for banks in advanced economies as well as in India, is an important driver of credit growth. Several definitions are considered to determine the robustness of the results. First capitalization is defined in turn as either common equity over total assets, total equity over total assets, or regulatory Tier 1 capital over total assets. The fourth measure of bank-level capitalization is the capital adequacy ratio, defined as Tier 1 regulatory capital over risk weighted assets. Figure 7 shows the path of bank-level capitalization overtime for public banks (PSBs) and private banks, as defined by the simple ratio of equity to assets and by the capital adequacy ratio. While median bank capitalization was volatile and slightly higher for private banks in the earlier years of the sample, since 2010 the gap between private and public banks has widened, though both have been trending upwards in recent years. Similarly, there has been a notable upward shift in the capital adequacy ratio since 2012, when India announced its intended adoption of the Basel III requirements (recommending a 9 percent capital adequacy ratio), aimed to be implemented in 2018–19. 6

Bank-level capitalization

As has been documented in the literature, while banks may use their capital to fund lending, given the relatively low share of capital on their balance sheets it is more likely that lending is funded through debt liabilities. This also appears to be in the case for Indian banks, as depicted in Figure 8 , that capital makes up a relatively small share of both private banks and PSBs.

Bank balance sheet composition

At the same time, there is evidence of a relationship between bank equity and bank assets (a large part of which is lending) in India, as has also been identified for other countries (Gambacorta and Shin, 2018). This is shown by estimating the simple correlation between total assets and total equity, both at the bank,;’, year, t , level:

where the model, in turn, includes the vector* of bank-level control variables (return on assets, NPLs), a set of bank-fixed effects, α t , and a set of year fixed effects, γ t . The coefficient/? indicates the correlation between bank assets and bank equity, which estimate separately for private banks and PSBs. These correlation estimates are reported graphically in Figure 9 . Indeed, the results suggest that for private banks in India there is a correlation between assets and equity close to one, even after including the full set of control variables. That is, as in Gambacorta and Shin (2018) the hypothesis of unit elasticity between the two variables can not be rejected, meaning they move closely together overtime. However, given the low share of equity in bank funding, even though equity and assets move closely together it cannot be the case that increases in equity directly result in increases in lending. Furthermore, for PSBs, this correlation is much weaker once aggregate factors that affect all bank assets simultaneously are controlled for (via time fixed effects)..suggesting an even weaker relationship.

Correlation – Total Assets and Total Equity

Having established a strong correlation between bank assets (largely comprised of lending) and bank equity—at least for private banks—the question of whether there is a direct link between the capitalization of Indian banks and their lending growth, via debt funding, is formalized. The analysis proceeds in three steps, following the literature. First, asking whether a bank’s capitalization reduces its cost of funding—this is important as it was previously established that most lending is likely stemming from debt funding. Second, investigating whether capitalization not only decreases funding costs, but whether it is actually associated with an increase in debt funding. Figure 10 , panels A and B, show these two simple correlations, and suggest that for Indian banks, there is a strong association between higher bank capitalization, lower funding costs, and greater debt funding growth. Finally, as seen in panel C, there is a strong positive correlation between lending growth and capitalization. Together, these suggest that better capitalized banks lend more, possibly through a cheaper debt funding channel. Such a result would be consistent with the existing literature on international banks. In the next section, these relationships are formalized.

Bank capitalization, funding, and lending

Finally, the paper will look at the macro-level and attempt to formalize the relationship between credit growth with real GDP growth. Because the distinction between public and private banks is made in the bank-level analysis, it is important to also understand how each contributes to aggregate credit growth in India. Figure 11 shows that throughout the period under analysis, public banks have been responsible for the largest share of credit to the economy. However, since around 2013, private bank credit growth has been much faster than public bank credit growth, suggesting private banks are becoming an increasingly important player in the Indian banking sector. Figure 12 reports the aggregate correlation between real GDP growth and credit growth for each type of bank, with both showing relatively strong positive correlations. This relationship is explored more carefully in the next sections.

Aggregate bank credit to the economy

Real GDP growth and credit growth

The methodology for the bank-level analysis follows the approach of two closely related papers, Gambacorta and Shin (2018) and Muduli and Behera (2021) . It then extends the analysis to the macro-level to analyze the impact of bank lending on real GDP growth in India. The approach will take several stages. First, it examines whether bank capitalization leads to lower debt funding costs and higher debt funding—establishing whether the channel of debt funding for lending also exists in private and public banks in India in the sample period. Then, it turns to lending, to examine whether bank capitalization matters for lending, again distinguishing between private and public banks. Finally, it looks at the aggregate and examines whether bank lending is correlated with higher real GDP growth in India. This latter step raises questions of causality—namely, whether lending boosts real GDP (for instance by increasing consumption and investment) or whether lending rises when real GDP growth is higher. Many papers have tried to tease out this relationship using data from other countries. While this paper has insufficient data to carefully establish causality (only a correlation), it will nonetheless argue that the approach suggests there is a likely channel of transmission from bank lending to real GDP growth in India.

To estimate the role of bank capitalization on funding costs, debt funding costs of bank i in period t, cost it , defined as the average cost of funding given by total interest rate paid overtotal level of debt (excluding equity and reserves), is regressed on bank capitalization (Capitalization it-1 ) , using various definitions described in the previous section. Time fixed effects and bank level controls, X it-1 , including return on assets, total assets, and the NPL ratio, are also included:

The model is estimated using the dynamic Generalized Method of Moments (GMM) estimator (Arellano and Bond, 1991), which ensures efficiency and consistency of the estimates. This is useful in this setting since the outcome variable likely depends on past realizations of itself. It is important to note that while this regression model can inform on the relationship between bank capitalization and funding costs, it cannot identify a causal relationship between these variables. Consistent with existing literature, it is expected that the results will show that lower capital levels are associated with higher prices for debt funding (i.e . higher equity reduces the cost of debt or that well capitalized banks pay less for their funding).

Having established a link between bank capitalization and the cost of funding, the analysis then estimates the impact of bank capitalization on funding levels, using a similar set-up, with the dependent variable this time the growth of debt funding, funds it :

In this case, it is expected that better capitalization and an increase in asset quality will increase the rate of debt funding.

The final step in the bank-level analysis estimates the impact of bank capitalization on credit supply, again in a similar setup as equations (3) and (4):

In this case, it is expected that better capitalization increases the growth rate of loans.

As a robustness exercise, the models in equations (3) -(5) are estimated via panel fixed effects estimation, which allow for the inclusion of both year and bank time fixed effects. The results for these exercises are reported in Annex Table 3 – 6 .

With bank-level results established, the analysis turns to addressing the question of what the relationship between banking lending, through bank balance sheets, is with the macroeconomy in India. This remains an open question because, while there is evidence that higher credit growth is often associated with higher GDP growth, in emerging markets this is sometimes the result of a boom-bust cycle which can ultimately lead to lower growth. In such a case, it may indeed be that the health of bank balance sheets is particularly important to avoid these extreme swings. Also motived by the results from the GaR model, a measure of balance sheet health is controlled for directly, defined using the NPL ratio. The following regression model is estimated to determine the relationship between real GDP growth and credit growth (at the bank-year, it , level) in India:

where the set of control variables are macro controls, including inflation, the real effective exchange rate, and world GDP growth. NPLs are defined as a dummy variable, equal to one if bank i’s NPL ratio in year t is below the sample mean. Credit growth, in turn, is defined as actual credit growth or as a dummy variable for high credit growth equals to one if bank i’s credit growth ratio in year t is above the sample mean. The credit growth variable is also winsorized at the 1 st and 99 th percentile, to account for extreme outliers. 7 Given the potential endogeneity between credit growth and GDP growth, this regression is unable to identify a causal relationship between the two variables but rather speaks to their correlation. Furthermore, given that we examine output growth at the aggregate level (GDP growth) we are estimating an average effect of credit growth over all bank characteristics – for instance, type of bank (public versus private) and size of bank. We address this averaging effect by examining split samples along various characteristics. With these caveats in mind, the next section presents the results.

The first results, based on estimating equation (4), are reported in Table 2 . The sample is split between public banks (columns 1 to 4) and private banks (column 5 to 8) and results are shown for the four different measures of bank capitalization. The results suggest that higher capitalization is associated with lower debt funding costs, especially and more so for private banks. This is consistent with what Gambacorta and Shin (2018) find for advance country banks. Muduliand Behera (2021) find a related, nuanced result for India, that (consistent with the results presented in this paper) a higher level of bank capital is associated with lowerfunding costs but for public banks it is only associated with lowerfunding costs if they have lower non-performing assets. In contrast, the results here indicate there is some negative association on average, regardless of the level of NPLs, but it is not as strong as for private banks. This could be because public banks often get public capital infusions, thus limiting the extent to which capital is indicative of risk for public banks.

Bank capitalization and cost of debt funding

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Cost of funding | ||||||||

| -0.0177 (0.0138) | -0.0260*** (0.00777) | |||||||

| 363 | ||||||||

| Yes | ||||||||

| Bank controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

Next, the analysis asks whether capitalization matters for the overall growth of debt funding. The results for estimating this, as indicated in equation (5), are reported in Table 3 , again separately analyzing public and private firms. Again, there is a similar distinction between the role of capitalization in public versus private banks. Private banks that have greater capitalization are associated with large, and significantly greater debt funding growth. For public banks, the relationship is less robust across the different measures of capitalization but there does seem to be a positive, albeit smaller, relationship.

Bank capitalization and debt funding growth

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Growth in debt funding | ||||||||

| 0.947*** (0.256) | 1.393*** (0.323) | |||||||

| 363 | ||||||||

| Yes | ||||||||

| Bank controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

The above established that better capitalized Indian (private) banks are able to find cheaper debt funding and raise more funds relative to less well capitalized banks, and this can be a source of funds for lending. The final exercise is to examine banks’ lending practices directly. Table 4 reports results from estimating equation (6). With respect to private banks, there is some evidence of a positive relationship between capitalization and lending. For public banks, no such evidence is found. Isolating the period from 2010–21, which is both when the RBI adopted the Basel II regulations and when private banks became much more prominent in India, delivers an even stronger positive relationship between capitalization and lending, as shown in Table 5 . Together, the results suggest that credit growth in India can be supported by ensuring banks are adequately capitalized, which enables them to raise more debt funding, at cheaper rates, which is then ultimately used to support lending growth. This relationship is, however, specific to private banks and does not seem to hold for public banks, which may have different funding models and different ability to lend.

Bank capitalization and lending growth

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Growth of gross loans | ||||||||

| 0.369 (0.294) | 0.805** (0.349) | |||||||

| 363 | ||||||||

| Yes | ||||||||

| Bank controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

Bank capitalization and lending growth, 2010–21

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Growth of gross loans | ||||||||

| 0.432 (0.888) | 1.369*** (0.335) | |||||||

| 165 | ||||||||

| Yes | ||||||||

| Bank controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

Turing to the macro-level results, reported in Table 6 , columns (3) and (4) suggest that there is a strong positive correlation between higher credit growth and real GDP growth, but only for those banks with a low NPL ratio. Furthermore, this result appears to be entirely driven by private banks (column (5)), with public banks (column (6)) showing no relationships between credit growth and real GDP growth regardless of the level of NPLs. Finally, the size of the bank (column (7)) does not appear to be related to whether credit growth is associated with higher GDP growth. 8

Real GDP Growth and Credit Growth

| Sample period 1990–2021 | |||||||

|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | |

| 0.884* (0.519) | 3.069*** (0.762) | ||||||

| -1.532 (0.936) | -0.610 (1.399) | ||||||

| 1.797* (0.961) | -0.00683 (1.345) | ||||||

| -0.293*** (0.0615) | -0.411*** (0.0894) | ||||||

| -0.199*** (0.0330) | -0.0682 (0.0517) | ||||||

| 0.348*** (0.0276) | 0.318*** (0.0403) | ||||||

| 5.753*** (0.237) | 5.727*** (0.340) | 5.807*** (0.237) | 25.73*** (3.405) | 32.00*** (4.740) | 13.01** (5.298) | 41.78*** (10.61) | |

| 588 | 279 | ||||||

| R-sq | 0.035 | 0.051 | 0.069 | 0.381 | 0.410 | 0.412 | 0.382 |

While the methodology used here cannot speak to the reason for the lack of relationship between public banks’ lending and growth, the reasons could be varied: public banks may have different objectives than private banks, and often engage in directed lending (also known as priority sector lending); the results could also reflect implicit guarantees that public banks have from the government. The result is also consistent with a large literature that finds publicly owned banks are generally associated with lower employment and growth (see, for instance, Carvalho, 2014 and La Porta et al., 2002 ). If real GDP growth is the overarching objective, then the results suggest private bank lending by banks with healthy balance sheets should be promoted. There may nonetheless be alternative reasons for continuing to promote public bank lending. It is also important to recall that this methodology does not speak to a causal relationship between bank lending and real GDP growth. The positive correlation may imply that private bank credit growth from banks with low NPLs spurs real growth, but it may also indicate procyclical lending by private banks (and countercyclical lending by public banks). Further analysis with micro-level data would be needed to disentangle this relationship, which is left to future research. Finally, the results presented here abstract from any lending by non-banks, which represent a large share of credit in India and may themselves also be important for real GDP growth. 9

- D. Policy Implications

Results from this panel regression analysis, as with the results from the GaR, highlight the importance of ensuring adequate credit growth and improving bank balance sheets, particularly through reducing NPLs, to boost growth. It is only those banks with low NPLs and high credit growth that are associated with higher GDP growth.

At the bank level, to ensure high credit growth, it is also imperative that banks are well capitalized. This allows them access to more and cheaper debt funding, which is in turn used to fund lending. These relationships, however, seem to exist primarily for private banks. Public banks, which may have different motivations for lending, appear to be less affected by their capital position in terms of their ability to lend.

Looking ahead, efforts to clean up bank balance sheets and boost capitalization—especially for private banks—will be critical in boosting credit growth, and thus GDP growth over the medium term.

- IV. Conclusions

This paper has examined the nexus between India’s financial sector and economic growth. It highlights the important role of financial sector on growth outcomes. Using two distinct methodologies, the results provide consistent messages. On a cyclical basis, a negative shock to credit and leverage or a rise in macro vulnerability all shift the distribution of growth to the left, with lower expected growth and higher negative tail risks, implying lower expected growth and higher downside risks. Over the long term, the results indicate that higher credit growth, arising from better capitalized banks with lower NPLs, is associated with higher GDP growth.

Together, these results point to several policy considerations. First, the results highlight the importance of ensuring adequate credit growth and improving the balance sheets of banks, particularly through reducing problem loans. During periods of low economic growth, policies to support credit growth and to strengthen balance sheets would be particularly important. Additionally, a focus on ensuring that private banks are well capitalized, either through new equity issuance or reducing cash dividends, is crucial, given the relationship between their balance sheets and credit to the economy. Finally, given the differences in results between private and public banks, efforts to better understand the drivers of this difference and address it could help promote growth.

Adrian , Tobias , Nina Boyarchenko , and Domenico Giannone , 2019 . “ Vulnerable Growth .” American Economic Review , Vol 109 ( 4 ): 1263 – 89

- Search Google Scholar

- Export Citation

Adrian , Tobias , Federico Grinberg , Nellie Liang and Sheheryar Malik , 2018 . “ The Term Structure of Growth-at-Risk .” IMF Working Paper 2018/180 .

Ang , Andrew , Monika Piazzesi , and Min Wei ( 2006 ). “ What does the yield curve tell us about GDP growth? ,” Journal of Econometrics, Elsevier , Vol. 131 ( 1–2 ), pages 359 – 403 .

Carvalho , Daniel , 2014 , “ The Real Effects of Government-Owned Banks: Evidence from an Emerging Market ,” Journal of Finance , 69 ( 2 ), pp. 577 – 609 .

Claessens , Stijn , Ayhan Kose , and Marco Terrones . 2011a . “ Financial Cycles: What? When? How? ” CEPR Discussion Paper 8379 , Centre for Economic Policy Research , London .

Claessens , Stijn , Ayhan Kose , and Marco Terrones . 2011b . “ How Do Business and Financial Cycles Interact? ” CEPR Discussion Paper 8396 , Centre for Economic Policy Research , London

Demirguc-Kunt , Asli and Ross Levine , 2018 . “ Finance and Growth ”, , Volume 1 , Edward Elgar Publishing .

Gambacorta , Leonardo and Hyun Song Shin , 2016 . “ Why bank capital matters for monetary policy ”, BIS Working Paper 558 .

Goodhart , Charles and Boris Hofmann , 2008 . “ House prices, money, credit, and the macroeconomy ,” Oxford Review of Economic Policy , Oxford University Press , Vol. 24 ( 1 ), pages 180 – 205 , spring .

International Monetary Fund , 2017 . “ Global Financial Stability Report .” Washington , October 2017.

La Porta , Rafael , Florencio Lopez-de-Silanes , and Andrei Shleifer , 2002 , “ Government ownership of banks ,” Journal of Finance 62 , pp. 265 – 302 .

Levine , Ross , 2005 . “ Finance and Growth: Theory and Evidence ,” Handbook of Economic Growth , in: Philippe Aghion & Steven Durlauf (ed.), Handbook of Economic Growth , edition 1 , volume 1 , chapter 12, pages 865 – 934 , Elsevier .

Muduli , S. and Behera , H. , 2021 . Bank capital and monetary policy transmission in India . Macroeconomics and Finance in Emerging Market Economies , pp. 1 – 25 .

Prasad , Ananthakrishnan , Selim Elekdag , Phakawa Jeasakul , Romain Lafarguette , Adrian Alter , Alan Xiaochen Feng and Changchun Wang , 2019 . “ Growth at Risk: Concept and Application in IMF Country Surveillance ,” IMF Working Papers 2019/036 , International Monetary Fund .

Seth , Gaurav , Supriya Katti and B.V. Phani , 2022 . “ Stock Price Reaction on the Announcement of Basel Implementation: Evidence from Indian Banks ” Reserve Bank of India Working Paper No. 1

- Annex I. Tables

Definitions and Data Sources of Macro-Financial Variables

| Variables | Definitions | Sources |

|---|---|---|

| Real GDP Growth | Real GDP at Market Prices, % Change – YoY | |

| Policy Rate | Repo Rate (EOP, % per annum) | |

| Treasury bill yields (10 year) | 10-Year Government Bond Yield (EOP, % per annum) | |

| Sovereign spreads | JPSSGINB Index | |

| Stock price change | Stock Prices: BSE Sensex/BSE 30 Index (% YoY) | |

| Inflation Rate | Consumer Price Index % Change – YoY | |

| Current account deficit | BOP: Current Account Balance / Real GDP at Market Price Haver Analytics/ Central Statistics Office and Reserve Bank of India | |

| Short term external debt to reserve ratio | Short-Term Gross External Debt / Intl Liquidity Reserves | |

| NPL ratio | Non-Performing Loans to Total Gross Loans (EOP, %) | |

| Credit growth | Adj Credit by All Sectors to Nonfin Priv Sector (% YoY) | |

| Credit to GDP Ratio | Adj Credit to the Private Nonfinancial Sector (% of GDP) | |

| Credit to GDP gap | Private Nonfinancial Credit to GDP Gap (EOP, %) | |

| World GDP growth | Real GDP, seasonally adjusted, % YoY, World | |

| Oil price change | West Texas Intermediate ($/Barrel) (% YoY) | |

| Exchange rate change | India: Rupee/US$ Exchange Rate (AVG) (% YoY) | Haver Analytics/ Reserve Bank of India |

Definitions and Data Sources of Panel Regression Variables

| Variable | Definition | Source |

|---|---|---|

| Leverage ratio (total equity) | Total equity divided by total assets (%) | |

| Leverage ratio (common equity) | Total common equity divided by total assets (%) | |

| Leverage ratio (Tierl) | Tier 1 capital divided by total assets (%) | |

| Capital adequacy ratio | Tier 1 capital divided by risk-weighted assets (%) | |

| Cost of funding | Total interest expense divided by total debt funding excluding derivatives | |

| Debt funding growth | Growth rate of debt funding | |

| Growth of gross loans | Growth rate of gross loans (%) | |

| Return on assets | Net income divided by total assets (%) | |

| NPL | Total impaired loans divided by gross loans | |

| GDP growth | Real GDP growth (%) | |

| Policy rate | Repo rate (average %) | |

| Real effective exchange rate | Real effective exchange rate against 10 currency basket | |

| Exchange rate | Rupee/USD exchange rate, nominal | |

| US Policy rate | Effective Fed Funds Rate | Haver |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Cost of funding | ||||||||

| -0.0205 (0.0144) | -0.0229** (0.00999) | |||||||

| 384 | ||||||||

| 0.872 | ||||||||

| Yes | ||||||||

| Yes | ||||||||

| Bank controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Growth in debt funding | ||||||||

| 0.649* (0.339) | 1.212 (0.835) | |||||||

| 384 | ||||||||

| 0.579 | ||||||||

| Yes | ||||||||

| Yes | ||||||||

| Bank controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Growth of gross loans | ||||||||

| 0.431 (0.327) | 0.741* (0.434) | |||||||

| 384 | ||||||||

| 0.645 | ||||||||

| Yes | ||||||||

| Yes | ||||||||

| Bank controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| PSBs | Private banks | |||||||

| 0.0812 (0.927) | 1.407*** (0.299) | |||||||

| 184 | ||||||||

| 0.692 | ||||||||

| Yes | ||||||||

| Yes | ||||||||

| Bank controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

Foreign bank capitalization and funding costs, debt, and lending growth

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Cost of funding | Growth in debt funding | Growth of gross loans | ||||||||||

| 0.00960 (0.0207) | -0.127 (1.473) | -7.719 (19.36) | ||||||||||

| 83 | 78 | |||||||||||

| Yes | Yes | |||||||||||

| Bank controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

- Annex II. Figures

Robustness Check – Growth-at-Risk: Shock to Credit and Leverage (Bank Credit)

Robustness Check-Growth-at-Risk: Term Structure for Credit Indicators (Bank Credit)

For a discussion of this broader topic, see Demirguc-Kunt and Levine (2018) and references therein.

The credit-to-GDP gap is based on BIS calculations, defined as the difference between the credit-to-GDP ratio and its long-term trend. According to the BIS, the long-term trend is computed using a one-side Hodrick-Prescott filter with lambda equal to 400,000, as credit cycles are on average longer than standard business cycles. For detailed methodology, please see Recent enhancements to the BIS statistics.

The first principal component of the credit and leverage partition (comprised of the credit -to-GDP ratio, the credit-to-GDP gap, credit growth, and the NPL ratio)captures77 percent of the variance.

We focus on domestic banks only as they have the best data coverage.

See Seth et al. (2022) for a timeline on India’s adoption of the Basel recommendations.

Results are robust to not winsorizing and available upon request.

The results for bank size are robust to defining a large bank as those with total assets in the top 25 and top 10 percent of the distribution of banks’total assets.

Results for foreign banks are presented in Annex Table 7 . While generally robust to the main results on private sector banks, the sample of foreign banks is relatively small, and thus difficult to assess with any precision the quality of the results.

Same Series

- Growth at Risk: Concept and Application in IMF Country Surveillance

- The Term Structure of Growth-at-Risk

- Financial Conditions and Growth at Risk in the ECCU

- Macrofinancial Linkages and Growth at Risk in the Dominican Republic

- Credit Growth and Economic Recovery in Europe After the Global Financial Crisis

- Linkages Between Financial Variables, Financial Sector Reform and Economic Growth and Efficiency

- The Long Shadow of the Global Financial Crisis: Public Interventions in the Financial Sector

- Financial Development and Economic Growth

- Macro-Financial Linkages in Egypt: A Panel Analysis of Economic Shocks and Loan Portfolio Quality

- Private Sector Deleveraging and Growth Following Busts

Other IMF Content

- CHAPTER 2 Financial Sector and Economic Growth

- Loose Financial Conditions, Rising Leverage, and Risks to Macro-Financial Stability

- A Monitoring Framework for Global Financial Stability

- PART I Setting the Stage and Overview

- West African Economic and Monetary Union: Financial Sector Assessment Program-Technical Note-Stress Tests, Credit Concentration, and Interest Rate Risks

- France: Financial Sector Assessment Program-Technical Note-Nonfinancial Corporations and Households Vulnerabilities

- Philippines: Financial Sector Assessment Program-Technical Note on Risk Assessment of Banks, Non-Financial Corporates, and Macro-Financial Linkages

- 2021 Financial Sector Assessment Program Review—Background Paper On Quantitative Analysis

- 4 Financial Sector Evolution: Challenges in Supporting Macroeconomic Stability and Sustainable Growth

- Euro Area Policies: Financial Sector Assessment Program Technical Note—Systemic Risk Analysis

Other Publishers

Asian development bank.

- ADB Economics Working Paper Series No. 573: Quarterly Forecasting Model for India's Economic Growth, Bayesian Vector Autoregression Approach

- A Study of Nonbanking Financial Companies in India

- ADB Economics Working Paper Series No. 562-Skewed Credit and Growth Dynamics after the Global Financial Crisis

- The Hybrid Annuity Model for Public-Private Partnerships in India's Road Sector: Lessons for Developing Asia

Inter-American Development Bank

- Is there a Caribbean sclerosis?: stagnating economic growth in the Caribbean-Chapter 5, Weak Institutions and Private Sector, IDB 2014

- Regional Financial Development and Firm Growth in Peru

International Fund for Agricultural Development

- The effect of the sectoral composition of economic growth on rural and urban poverty.

International Labour Organization

- Wage-led growth: An equitable strategy for economic recovery

The World Bank

- Banking Sector Openness And Economic Growth

- Financial dependence, banking sector competition, and economic growth

- India Financial Sector Assessment Program Update: Securities Regulation.

- India Financial Sector Assessment Program: Detailed Assessment of Observance of Clearing Corporation of India Limited Central Counterparty and Trade Repository

- Finance, Financial Sector Policies, and Long-Run Growth

- India Financial Sector Assessment Program: Basel Core Principles for Effective Banking Supervision.

- Is India's Economic Growth Leaving the Poor Behind?

- India's Growth Story

- India's Economic Growth and Environmental Sustainability: What are the Tradeoffs?

- India Economic Update, March 2012

- Share on facebook Share on linkedin Share on twitter

Table of Contents

- View raw image

- Download Powerpoint Slide

International Monetary Fund Copyright © 2010-2021. All Rights Reserved.

- [195.158.225.230]

- 195.158.225.230

Character limit 500 /500

Thank you for visiting nature.com. You are using a browser version with limited support for CSS. To obtain the best experience, we recommend you use a more up to date browser (or turn off compatibility mode in Internet Explorer). In the meantime, to ensure continued support, we are displaying the site without styles and JavaScript.

- View all journals

- Explore content

- About the journal

- Publish with us

- Sign up for alerts

- 13 December 2023

Where science meets Indian economics: in five charts

- Andy Tay 0 &

- Jack Leeming

Andy Tay is a freelance writer in Singapore.

You can also search for this author in PubMed Google Scholar

You have full access to this article via your institution.

Download a PDF of this graphic

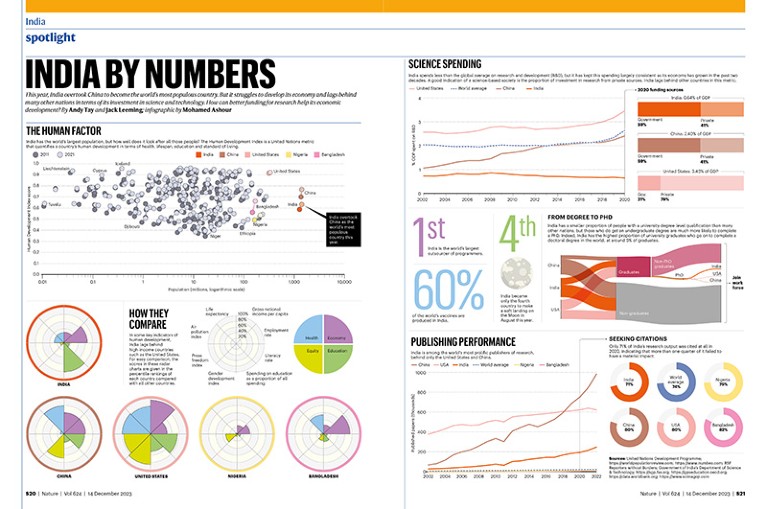

This year, India overtook China to become the world’s most populous country. But it struggles to develop its economy and lags behind many other nations in terms of its investment in science and technology. How can better funding for research help its economic development?

The human factor

India has the world’s largest population, but how well does it look after all those people? The Human Development Index is a United Nations metric that quantifies a country’s human development in terms of health, lifespan, education and standard of living.

Source: https://data.worldbank.org ; United Nations Development Programme. Infographic by Mohamed Ashour

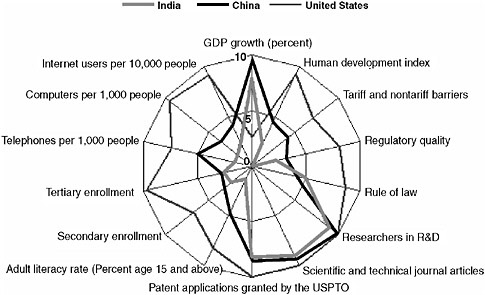

How they compare

In some key indicators of human development, India lags behind high-income countries such as the United States. For easy comparison, the scores in these radar charts are given in the percentile rankings of each country compared with all other countries.

Source: United Nations Development Programme; https://worldpopulationreview.com ; https://www.numbeo.com ; https://data.worldbank.org ; RSF Reporters without Borders. Infographic by Mohamed Ashour

Science spending

India spends less than the global average on research and development (R&D), but it has kept this spending largely consistent as its economy has grown in the past two decades. A good indication of a science-based society is the proportion of investment in research from private sources. India lags behind other countries in this metric. It is, however, the world’s largest outsourcer of programmers, and 60% of the world’s vaccines are produced in the country. And in August this year, India joined an exclusive club, becoming only the fourth country to make a soft landing on the Moon.

Source: https://data.worldbank.org ; https://sgp.fas.org ; Government of India’s Department of Science & Technology. Infographic by Mohamed Ashour

From degree to PhD

India has a smaller proportion of people with a university-degree-level qualification than many other nations, but those who do get an undergraduate degree are much more likely to complete a PhD. Indeed, India has the highest proportion of university graduates who go on to complete a doctoral degree in the world, at around 5% of graduates.

Source: https://gpseducation.oecd.org . Infographic by Mohamed Ashour

Publishing performance

India is among the world‘s most prolific publishers of research, behind only the United States and China.

Source: https://www.scimagojr.com ; https://data.worldbank.org . Infographic by Mohamed Ashour

Nature 624 , S20-S21 (2023)

doi: https://doi.org/10.1038/d41586-023-03907-5

This article is part of Nature Spotlight: India , an editorially independent supplement. Advertisers have no influence over the content.

Related Articles

- Developing world

Carbon pricing reduces emissions

News & Views 24 JUL 24

Megastudy shows that reminders boost vaccination but adding free rides does not

Article 26 JUN 24

Extending the Sustainable Development Goals to 2050 — a road map

Comment 17 JUN 24

Japan moves to halt long-term postgraduate decline by tripling number of PhD graduates

Nature Index 29 AUG 24

No more hunting for replication studies: crowdsourced database makes them easy to find

Nature Index 27 AUG 24

Can South Korea regain its edge in innovation?

Nature Index 21 AUG 24

No basis for claim that 80% of biodiversity is found in Indigenous territories

Comment 04 SEP 24

African scientists must not be priced out of mental-health research

World View 03 SEP 24

An ethical way forward for Indigenous microbiome research

Outlook 02 SEP 24

Postdoctoral fellow in computational biology

We are searching for a highly motivated postdoc interested in developing and applying computational approaches to understand how blood cell clones ...

Gothenburg (Kommun), Västra Götaland (SE)

University of Gothenburg

Faculty Positions in School of Engineering, Westlake University

The School of Engineering (SOE) at Westlake University is seeking to fill multiple tenured or tenure-track faculty positions in all ranks.

Hangzhou, Zhejiang, China

Westlake University

Postdoctoral Associate- Genetic Epidemiology

Houston, Texas (US)

Baylor College of Medicine (BCM)

NOMIS Foundation ETH Postdoctoral Fellowship

The NOMIS Foundation ETH Fellowship Programme supports postdoctoral researchers at ETH Zurich within the Centre for Origin and Prevalence of Life ...

Zurich, Canton of Zürich (CH)

Centre for Origin and Prevalence of Life at ETH Zurich

13 PhD Positions at Heidelberg University

GRK2727/1 – InCheck Innate Immune Checkpoints in Cancer and Tissue Damage

Heidelberg, Baden-Württemberg (DE) and Mannheim, Baden-Württemberg (DE)

Medical Faculties Mannheim & Heidelberg and DKFZ, Germany

Sign up for the Nature Briefing newsletter — what matters in science, free to your inbox daily.

Quick links

- Explore articles by subject

- Guide to authors

- Editorial policies

Current Issues in the Economy and Finance of India

- Conference proceedings

- © 2018

- Aswini Kumar Mishra 0 ,

- Vairam Arunachalam 1 ,

- Debasis Patnaik 2

Department of Economics, Birla Institute of Technology and Science (BITS), Pilani, Goa, India

You can also search for this editor in PubMed Google Scholar

Trulaske College of Business, School of Accountancy, University of Missouri, Columbia, USA

- Highlights innovative research on sustainable development, economics and finance in India

- Covers timely topics such as inflation dynamics, information transmission, leverage effect and volatility asymmetry, structural change and tax systems, among other

- Features contributions presented at the 2018 International Conference on Economics and Finance (ICEF)

Part of the book series: Springer Proceedings in Business and Economics (SPBE)

Included in the following conference series:

- ICEF 2018: International Conference on Economics and Finance

Conference proceedings info: ICEF 2018 2018.

8363 Accesses

14 Citations

This is a preview of subscription content, log in via an institution to check access.

Access this book

Subscribe and save.

- Get 10 units per month

- Download Article/Chapter or eBook

- 1 Unit = 1 Article or 1 Chapter

- Cancel anytime

- Available as EPUB and PDF

- Read on any device

- Instant download

- Own it forever

- Compact, lightweight edition

- Dispatched in 3 to 5 business days

- Free shipping worldwide - see info

- Durable hardcover edition

Tax calculation will be finalised at checkout

Other ways to access

Licence this eBook for your library

Institutional subscriptions

About this book

This proceedings volume highlights important points of achieving a balanced and sustained growth path from diverse economics and finance perspectives, touching on a wide array of economic and social analyses in India. Featuring contributions presented at the 2018 International Conference on Economics and Finance (ICEF-2018) held at the Birla Institute of Technology and Science, Pilani, Goa, India, the enclosed papers explore topics such as inflation dynamics, information transmission in post-recession era, leverage effect and volatility asymmetry, structural change and economic growth and reforming tax systems, among others.

Similar content being viewed by others

Macroeconomic Overview of the Indian Economy

Introducing the Volume on India’s Contemporary Macroeocnomic Themes-Looking Beyond 2020

The Impossible Trinity: Where Does India Stand?

- Indian Finance

- Indian Economics

- Agricultural Economics

- Rural Livelihood Programs

- India’s Service Trade

- Public Sector Banks in India

- Private Sector Banks in India

- Health Economics in India

- Ecotourism in India

- Heritage Communism

- Indian Stock Market

- India and the ASEAN

- Rural Wage Dynamics in India

- Human Capital Formation

- Economic Globalization in India

Table of contents (16 papers)

Front matter, globalization, macroeconomic performance and monetary policy, core inflation dynamics and impact of demand and supply shocks: evidence from india.

- Priyanka Sahu, Naresh Kumar Sharma

Demand for Money in India: An ARDL Approach

- Abdul Rishad, Akhil Sharma, Sanjeev Gupta

Some Empirical Evidence on the Effects of Monetary Policy in India: A Vector Autoregressive Based Analysis

- Gyanendra Pratap Singh

Stock Indices and Inflation Through Industry Prisms

- Abha Mohan, Tomy Mathew, K. Subramanian

Fundamental Drivers of Indian Stock Market

- Rubina Barodawala, Diksha Ranawat

Financial Institutions, Instruments and Markets

Information transmission in post-recession era: evidence from india, china, hong kong and japan.

- Ashish Kumar, Swati Khanna

A Statistical Re-assessment of Capital Adequacy and Insolvency Risk in Commercial Banks of India

- Nupur Moni Das, Joyeeta Deb

Examining the Linkages Between Financial Development and Energy Consumption in India

- Seema Saini, Yadawananda Neog

Leverage Effect and Volatility Asymmetry

- Parthajit Kayal, S. Maheswaran

Regional Economic Development Issues

Structural change and economic growth in india—a state-wise analysis.

- Kshamanidhi Adabar, Trupti Mayee Sahoo

Financing MSMEs Rife with Problems—A Demand Side Analysis

- Chinmayee Sahoo, Alok Ranjan Behera

Impact of MGNREGS on Rural Labour Markets and Agriculture: A Study of Madhya Pradesh

- T. Prabhakara Reddy, V. Suresh Babu

Public Policy Economics and Analysis

Reforming tax systems: key policy considerations from south and south-west asia.

- Matthew Hammill, Jose Antonio Pedrosa-Garcia

Policy Implications for Financial Inclusion of Unskilled Labor Migrants: Insights from Goa

- Mridula Goel, Saurabh Nayak

Income and Expenditure Mismatch of Poorest of the Poor: An Analysis of Financial Requirement of Slum Dwellers

- Firdous Ahmad Malik, D. K. Yadav, Ranu Jain

Other volumes

Editors and affiliations.

Aswini Kumar Mishra, Debasis Patnaik

Vairam Arunachalam

Bibliographic Information

Book Title : Current Issues in the Economy and Finance of India

Book Subtitle : ICEF 2018

Editors : Aswini Kumar Mishra, Vairam Arunachalam, Debasis Patnaik

Series Title : Springer Proceedings in Business and Economics

DOI : https://doi.org/10.1007/978-3-319-99555-7

Publisher : Springer Cham

eBook Packages : Economics and Finance , Economics and Finance (R0)

Copyright Information : Springer Nature Switzerland AG 2018

Hardcover ISBN : 978-3-319-99554-0 Published: 14 September 2018

Softcover ISBN : 978-3-030-07610-8 Published: 26 December 2018

eBook ISBN : 978-3-319-99555-7 Published: 13 September 2018

Series ISSN : 2198-7246

Series E-ISSN : 2198-7254

Edition Number : 1

Number of Pages : XXVII, 284

Number of Illustrations : 21 b/w illustrations, 17 illustrations in colour

Topics : Asian Economics , Regional/Spatial Science , International Economics , International Finance

- Publish with us

Policies and ethics

- Find a journal

- Track your research

Current World Environment

An international research journal of environmental science.

ISSN:0973-4929, Online ISSN:2320-8031

Views: 1950

PDF Downloads: 58

Climate Change and the Indian Economy - A Review

DOI: http://dx.doi.org/10.12944/CWE.17.1.3

Copy the following to cite this article:

Sharma M, Singh R, Kathuria A. Climate Change and the Indian Economy - A Review. Curr World Environ 2022;17(1). DOI: http://dx.doi.org/10.12944/CWE.17.1.3

Copy the following to cite this URL:

Sharma M, Singh R, Kathuria A. Climate Change and the Indian Economy - A Review. Curr World Environ 2022;17(1). Available From:

Select type of program for download

| EndNote format (Mac & Win) | |

| Ris format (Win only) | |

| Ris format (Win only) | |

| RefWorks format (Mac & Win) | |

| BibTex format (Mac & Win) |

Article Publishing History

| Received: | 25-10-2021 |

|---|---|

| Accepted: | 14-03-2022 |

| Reviewed by: | |

| Second Review by: | |

| Final Approval by: |

Introduction For a developing nation like India, climate change is a harsh reality. This is mostly because the backbone of the growth of a developing country is made of conventional methods of generating energy and resources. Despite a huge advancement in technologies, such countries often find themselves in conflicting positions. Economy, development and climate change often cross each other’s paths resulting in increased risk and vulnerability. This can be understood from the precipitation requirements and rainfall. For example, owing to climate change, in many areas the groundwater level has plummeted. This is the outcome of more than ever concrete surfaces diminishing the recharge rate of aquifers. 1 Indian agriculture rests on the support of groundwater and seasonal rainfall for the most part of the year. Consequently, the interplay of climate change and development factors has resulted in an acute water shortage for at least one month every year affecting a billion people in India while around 180 million suffer from severe water scarcity throughout the year. 2 Latterly, climatic variations disguised as cyclones and floods have caused massive desolation of crops, property, and infrastructure. This has also caused negative impacts on human health, especially heat stressors. Rural dwellers continue to depend on agriculture for livelihood and food, making them explicitly vulnerable to climate variability and change. All these factors hitch socio-economic development goals. 3,4 The national policies on climate change (“National Action Plan on Climate Change” (NAPCC)) are concentrated around human development and economic - industrial development policies. Local policies have helped in reducing urban air pollution levels. It is noteworthy that India is not responsible for rising temperatures despite contributing to 17.8% of the world’s population. It accounts for only 3.2% of cumulative emissions. 5 However, a report prepared by Deloitte Economics Institute, entitled “India’s Turning Point: How climate action can drive our economic future” projects that if the current practices and policies continue then India, may lose US$6 trillion in current value by 2050 that is 6% of the GDP in 2050 only. Averagely, in the next 30 years India will lose about 3% of GDP. This figure sores even more when we reach to 2070, wherein India will lose about US$35 trillion i.e., 12.6% of the GDP. 6 Yet, aspiring developmental goals without considering climate change is futile. At the same time, the huge and urgent developmental challenges cannot be ignored. Hence, both international efforts to alleviate the degree of climate change and domestic efforts to acclimatize the global warming already locked from earlier emissions. 7 The literature review on impact of climate change on economic development is quite overwhelming. It is not only in depth but also has good coverage. Although, literature pertaining to developing countries is not in abundance. However, it has been suggested that climate change do leave an impact on the economy and a transition to low carbon economy is possible only if the measures benefit economically. 8 Through this paper, we shall be highlighting how climate change is impacting the economy of India. Such nearly backward countries are not responsible for the large-scale emissions that are jeopardizing the present and future generations. While who is responsible or who is not for current climatic adversities, is very subjective. Herein, we shall be presenting why such immediate policy changes meet reluctance and how despite this India can reach its developmental goals in the long run. Materials and Methods This paper presents a qualitative research based on data extracted and analyzed from crucial government documents like “Assessment of Climate Change over the Indian Region Report 2020” and research papers. 9 Initially, we have tried to express the climate change briefly supported via facts and figures. Appropriate figures for time series analysis of temperature and monsoon have been included for a comprehensive interpretation of the trends from available data. Further we have given context to the pillars that make up the Indian economy and how they have been suffering as a consequence of climate change. We have emphasized on agriculture, livestock, infrastructure, and low-income households. Then we have discussed the energy needs that are crucial to development and how they present a difficult situation. We have discussed how meeting energy needs in developing countries leads to climate changes. Further we have stressed on how we can aspire for growth and development, even while keeping a check on climate change with valuable suggestions. Regional Indian Climate Change The climate of India is quite diversified in nature, from the Himalayan crown to the flat beaches, a significant transition in climate is visible. The climate varies from the freezing temperatures of the Himalayan Mountains to the tropical climatic conditions of southern India. The eastern states received the maximum rainfall while the western states dried of water make up the arid deserts of Thar and Great Indian Desert. Such a vastness of climatic conditions has always benefited India. However, in recent years many reports have projected the possibility of irreversible climatic changes. The IPCC 2021 report of climate change came as a shock for many as the report solidified its case of climatic worries and warned of severe consequences. For India too, in the past, many documents and reports have repeatedly shown the changing climatic trends and their impact on the Indian dimensions. The amplitude of the “CO 2 mixing ratio” has been rising gradually for the last few years. How has the climate so far changed…? Temperature A report on the assessment of Indian climate (“Assessment of Climate Change over the Indian Region Report 2020”) 9 has shown that the annual mean, minimum and maximum temperatures for the period of 1986-2015 have shown considerable warming by 0.15 °C, 0.13 °C, and 0.15 °C respectively. A significant change in pre-monsoon temperatures has also been seen with the highest warming trend. Heat extremes have increased over pan India during the period of 1951-2015. An ascending warming trend has been seen in the recent 30 years. An increase in the warmest day and warmest night temperatures along with the coldest night temperature has been observed since 1986. For India, an earlier IPCC report has forecasted the increased number of heat waves, and hot days. Deaths due to heat stress have also risen in recent years. 10 The Indian Ocean Sea Surface Temperature has been increasing with an average increase of 1.0 °C which was higher than the global average (0.7 °C) during 1951-2015. It has been speculated that around 90% of heating/warming is due to emissions caused by human activity and this will continue in the upcoming future in case of both high and medium emissions. 11

| |

The first graph is for largest maximum temperature for the months of March to May. The second graph is for the lowest minimum temperature for the months of December to February. The third graph is the difference between the two temperatures denoted for four major climate zones that are Bhubaneswar (blue line), Mumbai (green line), and Delhi (red line) during 1951-2015 and Chennai (black line) during 1980-2015. The calculations and graphical analysis have been done using Mann Kendall rank test with a 90% significance level. From the Figure 1, it can be observed that there is high variability in the minimum and maximum temperature in the later years (1981-2015). 12 These observations are in compliance with the theoretical data that has been published in climate assessment reports (Table 1). Below mentioned is tabular data for temperature increase for different months/seasons during a year. 13 Table 1: Temperature Trends for different Months/Seasons during the Years 1986 - 2015.

|

| C/ Decade) | ||

|

|

|

| |

| Annual | 0.15±0.09 | 0.13±0.10 | 0.15±0.10 |

| Winter (December - February) | 0.05±0.16 | 0.07±0.18 | 0.03±0.20 |

| Pre-Monsoon (March - May) | 0.26±0.17 | 0.20±0.16 | 0.29±0.20 |

| Monsoon (June - September) | 0.11±0.12 | 0.11±0.08 | 0.10±0.17 |

| Post- Monsoon (October - November) | 0.17±0.17 | 0.19±0.20 | 0.14±0.22 |

Rainfall As the temperature increases, its effect can be easily seen on the rainfall of the region. This is because warm air holds greater moisture in comparison to cold air and warm water evaporates at a faster pace. A cumulative effect of these is seen in the rain. These are causing more frequent heavy downpours which are not usually common. During the period of 1950 to 2015, there has been a threefold increase in heavy precipitation in the central Indian region. 14 While extreme precipitation has considerably risen over the subcontinent, however, an extremely contrasting observation has also been made. According to the assessment report, there has been an overall plummeting rainfall trend in the annual all-India and mean summer monsoon precipitation in the period of 1951 to 2015. This has been observed largely in the Western Ghats and Indo-Gangetic Plains. The cause for this trend is a notably increased concentration of anthropogenic (human-caused) aerosols over the northern hemisphere. Urbanization, improper land use, and increased anthropogenic aerosols are considered the main factor behind the increased localized rainfall and overall mean rainfall decrease. The time scale analysis of rainfall for the current year during the monsoon season from June to September depicts intense monsoon variability with frequent maximum peaks (Figure 2). As expected from theoretical research, the monsoon is becoming severe. India receives most of its rainfall from the monsoon. This exotic wind pattern has been responsible for a significant amount of rainfall over the Indian subcontinent. Hence, a major impact of climate change has been seen on this pattern. It has been projected that the monsoonal precipitation is going to become more severe in the future due to an increase in mixture content as a consequence of increased temperatures.