Access Key Navigation

- Skip to main navigation

- Skip to content

- Contact page

- Skip to search

Choose your country

- International

Europe, Middle East and Africa

- Czech Republic

- Liechtenstein

- Netherlands

- Saudi Arabia

- South Africa

- Switzerland

- United Kingdom

- United Arab Emirates

Asia-Pacific

- Greater China Region

- Philippines

- South Korea

- Cayman Islands

Country Selection

Choose your language.

About Us Press Release

Global Wealth Report 2022 – record wealth growth in 2021 tapered by challenging 2022 market environment

Further information

Imran Javaid Credit Suisse +44 207 883 0651 [email protected]

Media Relations Credit Suisse AG +41 844 33 88 44 [email protected]

Share Buttons

Wealth grew at a strong pace in 2021 and by year-end, global wealth at prevailing exchange rates totaled USD 463.6 trillion, a gain of 9.8%. Wealth per adult rose 8.4% to USD 87,489. Setting aside exchange rate movements, aggregate global wealth grew by 12.7% in 2021, which is the fastest annual rate ever recorded. However, factors such as inflation, rising interest rates, and declining asset price trends could reverse last year’s impressive growth in 2022.

2021 was a bumper year for household wealth driven by widespread gains in share prices and a favorable environment created by central bank policies in 2020 to lower interest rates, but at the cost of inflationary pressures. Rises in interest rates in 2022 have already had an adverse impact on bond and share prices and are also likely to hamper investment in non-financial assets. Inflation and higher interest rates could slow household wealth growth in the near term even if nominal gross domestic product (GDP) rises at the relatively rapid pace predicted for this year.

Key highlights

- Aggregate global wealth totaled USD 463.6 trillion at the end of the year, a rise of USD 41.5 trillion or 9.8%. Wealth per adult was up 8.4% to reach USD 87,489 at year-end. These amounts are reduced because they refer to US dollars at current exchange rates, and the US dollar appreciated during the year. If exchange rates had remained the same as in 2020, total wealth would have grown by 12.7% and wealth per adult by 11.3%.

- Accounting for inflation lowers the wealth growth rates. In 2021, the estimated increase in real wealth was +8.2%. As we look ahead toward a period of more elevated inflation than in the past two decades, the comparison of real and nominal wealth trends grows in relevance.

- All regions contributed to the rise in global wealth, but North America and China dominated, with North America accounting for a little over half the global total and China adding another quarter. In contrast, Africa, Europe, India and Latin America together accounted for just 11.1% of global wealth growth. This low figure reflects widespread depreciation against the US dollar in these regions. In percentage terms, North America and China recorded the highest growth rates (around 15% each), while the 1.5% growth in Europe was by far the lowest among the regions.

- Total household debt increased by 4.4% for the world as a whole. However, the global figure was suppressed by zero growth for the Asia-Pacific region (excluding China and India) and the reduction in debt in Europe (due to exchange rate depreciation). Elsewhere, household debt rose on average by 9%, led by a rise of 12.1% in China.

- A look at specific population sub-groups suggests that, in the United States and Canada, Millennials and Generation X grew their wealth most between 2019 and 2022. In the United States, African American and Hispanic households saw the largest percentage increase in wealth in 2021 thanks to increases in non-financial wealth – mostly housing. With regard to women’s wealth, it is estimated that, of the 26 countries that make up 59% of global adult population, 15 countries (including China, Germany and India, for example) show a decline in the wealth of women over 2020 and 2021. For the remaining countries (including the United States and the United Kingdom, for example), the average ratio of women to men’s wealth increased.

Global wealth levels 2021

- The most significant development in 2021 was the widespread and sizable gains in share prices.

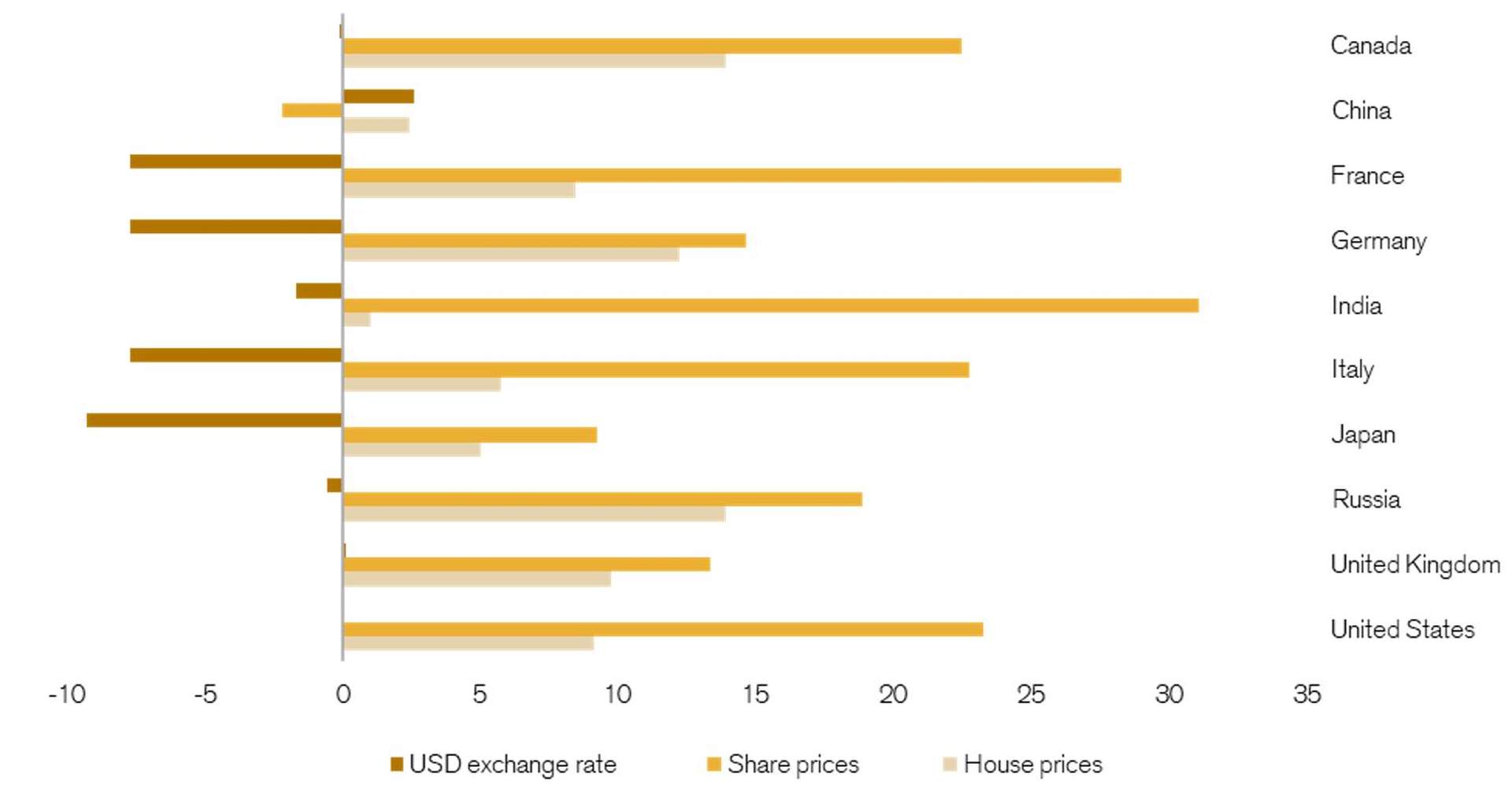

- Much of the year-on-year change in estimates of the household wealth of individual countries depends on asset prices and exchange rates. Among the countries covered in Figure 3 (G7 countries plus China, India and Russia), India led the way with a 31% rise, but France (28%), the United States (23%), Italy (23%) and Canada (22%) were not far behind. Elsewhere, share prices rose by more than 30% in Austria, Sweden, Saudi Arabia, Vietnam and Israel, and by more than 40% in Romania, Czechia and the UAE. In contrast, share prices fell by 2.2% in China, by 5%–6% in New Zealand, Chile and Pakistan, and by 17% in Hong Kong SAR.

Figure 2: Percentage change in USD exchange rate, share prices and house prices, 2020

- Exchange rate fluctuations are often the source of sizable gains and losses in wealth valued in US dollars. On average in 2021, countries depreciated against the US dollar by 2.9%. Among the countries covered in Figure 3, Japan (–9.3%) and the Eurozone (–7.7%) experienced the largest declines.

- Significant rises in GDP combined with vigorous equity and housing markets is highly likely to produce sizable wealth gains at the country level, and this was certainly the case in 2021. The United States added USD 19.5 trillion to its stock of household wealth. This is well above the second-place contribution of China (USD 11.2 trillion), which in turn far exceeds the rises recorded in Canada (USD 1.8 trillion), India (USD 1.5 trillion) and Australia (USD 1.4 trillion). In 2022, asset prices have fallen already and a tempering or partial reversal of the 2021 trend can be expected.

Wealth distribution 2021 The wealth share of the global top 1% rose for a second year running to reach 45.6% in 2021, up from 43.9% in 2019. US dollar millionaires gained 5.2 million extra members during 2021 and totaled 62.5 million worldwide at the year end. This 9% growth was slightly above the 8.4% increase recorded for wealth per adult, but fell short of the 9.5% rise in median wealth. The number of ultra-high-net-worth (UHNW) individuals expanded at a much faster rate, adding 21% new members in 2021. The United States (30,470) was the country that gained the most UNHW members, followed by China (5,200). UHNW membership also increased by more than a thousand in Germany (1,750), Canada (1,610) and Australia (1,350). Reductions in UHNW individuals were relatively uncommon. The biggest falls occurred in Switzerland (down 120), Hong Kong SAR (down 130), Turkey (down 330) and the United Kingdom (down 1,130).

An analysis of median wealth within countries and across the world shows that global wealth inequality has fallen this century due to faster growth achieved in emerging markets. Global median wealth has risen roughly twice as fast as global wealth per adult and much more rapidly than global GDP. The average household has thus been able to build up wealth over the last two decades.

Wealth outlook Worldwide inflation and the Russia-Ukraine war are likely to hamper real wealth creation over the next few years. Nevertheless, global wealth in nominal US dollars is expected to increase by USD 169 trillion by 2026, a rise of 36%. Low and middle-income countries currently account for 24% of wealth, but will be responsible for 42% of wealth growth over the next five years. Middle-income countries will be the primary driver of global trends. Global wealth per adult is forecast to rise 28% by 2026 and to pass the threshold of USD 100,000 in 2024. The number of millionaires will also grow markedly over the next five years to 87 million, while the number of UHNWIs will reach 385,000.

Axel Lehmann, Chairman of the Board of Directors of Credit Suisse Group AG and Chair of the Credit Suisse Research Institute , said: “We are very proud to present the thirteenth edition of our Global Wealth Report. As a leading wealth manager, it is a prerequisite for us to have a deep understanding of private wealth developments and share these with our stakeholders to help them navigate the future. As inflation is dominating the current investment discourse, this year’s study offers an additional assessment of real as opposed to nominal wealth trends to take account of the effect of inflation on global wealth.”

Anthony Shorrocks, economist and report author , said: “On a country basis, the United States added the most household wealth in 2021, followed by China, Canada, India and Australia. Wealth losses were less common and almost always associated with currency depreciation against the US dollar. Analysis of median wealth within countries and across the world shows that global wealth inequality has fallen this century due to faster growth achieved in emerging markets. The average household has thus been able to build up wealth over the last two decades.”

Nannette Hechler-Fayd’herbe, Chief Investment Officer for the EMEA region and Global Head of Economics & Research at Credit Suisse , said: “While some reversal of the exceptional wealth gains of 2021 is likely in 2022/2023 as several countries face slower growth or even recession, our five-year outlook is for wealth to continue growing. Higher inflation also yields higher forecast values for global wealth when expressed in current US dollars rather than real US dollars. Our forecast is that, by 2024, global wealth per adult should pass the USD 100,000 threshold and that the number of millionaires will exceed 87 million individuals over the next five years.”

The Global Wealth Report 2022 is available at: www.credit-suisse.com/researchinstitute

- Media Release ,

- Latest News

You are about to change the origin country from where you are visiting Credit-suisse.com.

Visit your regional site for more relevant services, products and events.

Continue to the site you have selected

Remain on your origin country* site

*The country of origin is defined in your browser settings and may not be identical with your citizenship and/or your domicile.

Explore our latest thought leadership, ideas, and insights on the issues that are shaping the future of business and society.

- Reshape our future with generative AI

- Leading sustainability

- The future of technology

- Marketing for customer experience

- Our research library

- Expert perspectives

Choose a partner with intimate knowledge of your industry and first-hand experience of defining its future.

- Aerospace and defense

- Banking and capital markets

- Consumer products

- Energy and utilities

- Hospitality and travel

- Life sciences

- Manufacturing

- Media and entertainment

- Public sector

Discover our portfolio – constantly evolving to keep pace with the ever-changing needs of our clients.

- Customer first

- Cybersecurity

- Data and artificial intelligence

- Enterprise management

- Intelligent industry

- Sustainability

Become part of a diverse collective of free-thinkers, entrepreneurs and experts – and help us to make a difference.

- Why join Capgemini

- Life at Capgemini

- Meet our people

- Back Career paths

- Students and graduates

- Experienced professionals

- Our professions

- Careers at Capgemini Engineering

- Careers at Capgemini Invent

- Back Join us

- Recruitment process

- Interview tips

See our latest news, and stories from across the business, and explore our archives.

- Press releases

- Analyst recognition

- Client stories

- Inside stories

- Social media

We are a global leader in partnering with companies to transform and manage their business by harnessing the power of technology.

- Back Who we are

- The way we work

- Our innovation ecosystem

- Values and Ethics

- Nobel International Partner

- Back Management and governance

- Board of Directors

- Executive committee

- Responsible business

- Environment, Social & Governance

- Back Corporate Social Responsibility

- CSR partnerships

- Digital inclusion

- Diversity and inclusion

- Environmental sustainability

- Back Transforming sports

- The America’s Cup

- Peugeot Sport

- World Rugby

- Technology partners

- Asia Pacific

- Europe & Middle East

Our number one ranked think-tank

Explore our brands

Explore our technology partners

Explore careers with our brands

Generative AI

Management team

World Wealth Report 2024

Intelligent strategies for winning with the ultra-wealthy: Bridge wealth management and family office strengths to fuel growth

Today’s global wealth management landscape is more challenging than ever: even as high-net-worth individual (HNWI) prosperity rebounds, geopolitical uncertainties, market volatility, and a fiercely competitive environment are putting pressure on global wealth and investment management industry profits.

The World Wealth Report 2024 reflects the views of 3,119 high-net-worth individuals, including 1,300+ ultra-high-net-worth individuals (UHNWI); 75 executives from pure wealth management (WM) firms, universal banks, broker/dealers, and family offices; and along with survey responses from 750+ relationship managers across North America, Europe, and Asia-Pacific. Key findings include:

- Rebounding markets and a brighter outlook lifted 2023 global HNWI wealth by 4.7%,1 and HNWI population numbers increased by 5.1%.2 While growth was seen across all wealth bands, the ultra-HNWI segment (investors with USD 30 million+) enjoyed the most robust recovery in dollar terms.

- By integrating behavioral finance with artificial intelligence, global wealth management firms can better recognize and address HNWI client needs; and Gen AI can aid hyper-personalization of relationship manager/client experiences and communications.

- Traditional global wealth management firms must balance competition and collaboration with family offices to scale up engagement with ultra-high-net-worth individuals: a collaborative ecosystem of partners to create a one-stop shop is key to success with this complex and lucrative client segment.

Download now

Thank you for your submission. download the report here ..

We are sorry, the form submission failed. Please try again.

World Wealth Report 2024 highlights

Highlight 1, global hnwi wealth and population take upward trajectories.

Solid economic resilience, cooling inflationary pressures, and recovering 2023 global markets drove growth as HNWI wealth and population surpassed the highs of 2021 in the aftermath of 2022 declines.

Highlight 2

High-net-worth individuals are cautiously optimistic about 2024 growth opportunities.

As cash and cash equivalents normalized to 25%, down from a multi-decade 34% high in 2023, alternative investments, real estate, and fixed income are gaining position in HNWI portfolio allocations. 2024 HNWI asset mix is rebalancing between preservation and growth

Highlight 3

Hnwi investment decisions are prone to biases.

While standard economic theory considers investors rational, humans are emotional and high-net-worth individuals are no exception. More than 65% of HNWIs said biases influence their investment decisions, especially during significant life events such as marriage, divorce, and retirement.

Highlight 4

Value-added services are crucial to win ultra-high-net-worth individuals.

With complex lifestyles and sophisticated needs, ultra-high-net-worth individuals prioritize value-added services, with 78% considering them essential to their wealth management firm relationships. UHNWIs are intense consumers of value-added services.

New wealth management strategies for high-net-worth individuals

Strategic and future-focused wealth management firms need to set their sights on retaining and winning ultra-high-net-worth individual clients’ mind share to boost their wallet share. But where should they begin?

- Ignite engagement with high-net-worth individuals as market trends evolve during high instability.

- Turbocharge AI-powered behavioral finance to enhance personalization and customer relationships.

- Focus on the highly concentrated and profitable ultra-high-net-worth individuals segment, and strike the right balance between competition and collaboration with family offices.

View prior World Wealth reports

World Wealth Report 2023 World Wealth Report 2022 World Wealth Report 2021

Integrated Wealth Management

Banking and Capital Markets

1 Capgemini Research Institute for Financial Services Analysis, 2024. 2 Capgemini Research Institute for Financial Services Analysis, 2024.

Disclaimers / Acknowledgments

The information in this report is general and not intended as legal, tax, investment, financial, or professional advice. Capgemini assumes no liability for errors or omissions or the use of this material. This report is for informational purposes only and may not address your specific needs. Capgemini disclaims responsibility for translation inaccuracies and provides the information “as-is,” without warranties. Capgemini will not be liable for any losses arising from reliance on this information.

Nilesh Vaidya

Global Head of Banking and Capital Markets

Marie Wattez

Global Head of Private Banking & Wealth Management

Global Head of Financial Services Applications Business Line

Carlos Salta

Global Head of Banking and Capital Markets Practice

Sandeep Kurne

Digital Core Banking & Wealth Management Portfolio Head

Maxime Gaudin

Head of Wealth and Asset Management Consulting, Europe

Elias Ghanem

Global Head of Capgemini Research Institute for Financial Services

Vivek Singh

Head of Banking and Capital Markets, Capgemini Research Institute for FS

Get in touch

Related research and insights.

Gaining HNWI market share: Embracing AI-powered behavioral finance

Wealth advising 2024: Key trends for success

Capturing wallet share: delivering on the uhnwi top 10 list.

Wealth management top trends 2024

Getting personal – five drivers to power client-centric growth in wealth management, client story.

International banking group grows customer engagement with investment research platform

Revenue growth driven by attracting more customers through a customer-centric digital research platform.

Stay informed

Subscribe to receive our financial services World Reports

Subscribe today

Thank you for subscribing., executive steering committee.

Michelle Owen

Global Head of Distribution, Global Private Banking

Pierre Ramadier

CEO, Wealth Management International Markets

BNP Paribas

Raymond Ang

Global Head, Private Bank and Affluent Clients

Standard Chartered

Barry Metzger

Managing Director, Income and Wealth Solutions

Charles Schwab

Kabir Sethi

Wealth Management Leader

Ex-LPL Financial

Greg Gatesman

Head of International Client Development, Wealth Management Americas

Nic Dreckmann

Julius Baer

Michel Longhini

Group Head, Global Private Banking

First Abu Dhabi Bank

Ranjit S Samra

Head of Product & Experience

J.P. Morgan Wealth Management

Philippe Perles

Committee Member

Association of Swiss Asset and Wealth Management Banks

WealthTech Expert

MFO Founder and Family Office

G Consult Finances

Christian Stadtmüller

Managing Director

Sébastien Capt

Prime Partners

Christine Ciriani

Head of International Digital Wealth

InvestCloud

Head of Global Banking Solutions

Noah Kraehenmann

Global MD Wealth Management

Arnaud Picut

Asking the better questions that unlock new answers to the working world's most complex issues.

Trending topics

AI insights

EY Center for Board Matters

Case studies

Operations leaders

Technology leaders

EY helps clients create long-term value for all stakeholders. Enabled by data and technology, our services and solutions provide trust through assurance and help clients transform, grow and operate.

EY.ai - A unifying platform

Strategy, transaction and transformation consulting

Technology transformation

Tax function operations

Climate change and sustainability services

EY Ecosystems

EY Nexus: business transformation platform

Discover how EY insights and services are helping to reframe the future of your industry.

How Microsoft built a new mobility model for cross-border talent

14 May 2024 EY Global

Private equity

How GenAI is empowering talent at a PE-backed consumer brand

09 May 2024 EY Global

Strategy and Transactions

How carve-outs positioned an automotive giant for future growth

12 Apr 2024 EY Global

We bring together extraordinary people, like you, to build a better working world.

Experienced professionals

EY-Parthenon careers

Student and entry level programs

Talent community

At EY, our purpose is building a better working world. The insights and services we provide help to create long-term value for clients, people and society, and to build trust in the capital markets.

Press release

Vellayan Subbiah from India named EY World Entrepreneur Of The Year™ 2024

07 Jun 2024 Eric J. Minuskin

Extreme E and EY publish Season 3 report, recording 8.2% carbon footprint reduction as female-male performance gap continues to narrow

09 Apr 2024 Michael Curtis

EY announces acceleration of client AI Business Model adoption with NVIDIA AI

20 Mar 2024 Barbara Dimajo

No results have been found

Recent Searches

Rethink customer experience as human experience

Technology will transform customer experience. Competitive differentiation will come from connecting to what is essentially human. Learn more.

How can trust survive without integrity?

The EY Global Integrity Report 2024 reveals that rapid change and economic uncertainty make it harder for companies to act with integrity. Read our findings.

How CEOs juggle transformation priorities – the art of taking back control

EY CEO survey highlights how CEOs consider AI transformation, ESG and M&A to navigate between immediate profits and future sustainability aspirations. Read more.

Select your location

The General Counsel Imperative

EY Global Forensic & Integrity Services Deputy Leader

- Link Copied

How can trust survive without integrity? (PDF)

The ey global integrity report 2024 reveals that rapid change and economic uncertainty make it harder for companies to act with integrity..

- Overall, integrity standards are improving; however, corporate misconduct appears to be on the rise.

- The gap between what leaders say about integrity versus how they act is growing, which perpetuates integrity risk within the organization.

- General counsel can help to build an integrity-first organization that puts people at the center.

T he EY Global Integrity Report 2024 (pdf) reveals some good news: Almost half (49%) of global respondents think compliance with their organization’s standards of integrity has improved in the last two years. This marks an increase of seven percentage points from our EY Global Integrity Report 2022 findings. However, headwinds continue:

- Nearly four out of 10 (38%) global respondents admit they’d be prepared to behave unethically in one or more ways to improve their own career progression — more than one and a half times higher than the findings in the last report.

- Employee misconduct is directly influenced by the behaviors they observe from leaders — where 25% of workers say they’d behave unethically for their own benefit, the percentage rises to 67% among board members and 51% among senior management.

- Leaders face pressure to look the other way on misconduct. Nearly two-thirds (65%) of board members and 57% of senior management feel under pressure not to report misconduct.

- A lack of training and awareness, and insufficient resources, open the door to misconduct. More than half (54%) of global respondents say that employees not understanding policies or requirements, combined with a lack of internal resources to manage compliance activities, creates opportunities for employees to violate integrity standards.

The General Counsel Imperative Series provides critical answers and actions to help leaders reframe the future of their organizations. The findings of the EY Global Integrity Report 2024 suggest that general counsel and chief compliance officers (CCOs) are seeing their roles and responsibilities expand. This is adding pressure to an increasingly long list of requirements and skills they need to keep current within a rapidly changing environment.

Integrity incidents are on the rise

One in five respondents admits that their organization has had a significant integrity incident, such as a major fraud, data privacy and security breach, or regulatory compliance violation, in the last two years. Notably, of those who say their organization had a significant integrity incident, more than two-thirds (68%) say the incident involved a third party.

An analysis of corporate violations in the US and the UK from 2010 to 2023 1 highlights the following:

- Almost US$1trillion in penalties have been incurred since 2010 (inflation adjusted), with over 40% growth in both the number of violations and the number of companies violating.

- Certain financial and employment violations have become two to 10 times more frequent since 2010, including accounting deficiencies, anti-money laundering (AML) deficiencies, tax violations, labor standards, workplace safety and consumer privacy.

- On the flip side, there has been a sharp drop in violations related to employee compensation, public safety, banking and the environment, and limited progress on anti-competitive behavior, discrimination or whistleblower retaliation.

- Repeat offending is linked to an erosion of culture. In instances where companies were repeat offenders, systemic issues within their compliance program or organization may not have been remediated or addressed. The number of different violation types steadily climbs from one in four companies with a violation in a single year up to 8.3 for those with a violation every year since 2010.

The gap between talk and action remains wide

The “say-do” gap is an issue we raised in the EY Global Integrity Report 2022. The latest findings suggest little has changed to close the gap between what leaders are saying about corporate integrity and what they are doing — or what their people are doing. This is especially concerning at the board level, where executives appear more likely to behave badly themselves and tolerate the behavior of potentially compromised employees if they are senior or high performers.

More than eroding (or erasing) trust within and outside the organization, a top-down, “all talk, no walk” mentality puts the organization’s reputation and bottom line at risk. One recent research finding suggests that US corporate fraud destroys roughly 1.6% of a company’s equity value annually, equal to US$830b in 2021. 2

Organizations can create a virtuous circle of integrity

In times of rapid change and difficult market conditions, it can be challenging for organizations to maintain or strengthen their standards of integrity. Arguably, this is exactly the time to make integrity a top priority. By taking an agile, human-centered approach to integrity — one that puts the right programs in place to drive behavior, to create a strong culture and a strong belief in their commitment to integrity — organizations can keep pace with evolving regulations and increasing societal expectations. Equally, they can create a virtuous circle of integrity that sets a course to renewed trust within the organization, and among customers, investors, government and society.

Is the value of integrity at risk?

Organizations need to improve their approach to integrity to maintain stakeholder trust.

The current state of integrity shows improvement

In emerging markets, 58% of respondents believe compliance has improved, which is a positive development given the inherent integrity and compliance risks experience in such markets.

Top reasons cited for improved integrity across all respondents globally suggest that improvements are coming both from better direction from management and leadership, and stricter regulation and pressure from regulators.

How EY can Help

Integrity and Compliance

As regulatory enforcement and public intolerance of corporate misconduct increase, EY professionals help you strengthen your integrity and global compliance frameworks. And, should violations occur or allegations of fraud or corruption arise, the EY Forensics teams help you respond quickly to safeguard your business.

Headwinds to sustain integrity are intensifying

However, respondents also admit that an increasingly complex integrity landscape makes it difficult to navigate legal and regulatory challenges. The research points to a number of key external and internal challenges:

- External risks: Nearly half (49%) of global respondents are finding it difficult to adapt to the speed and volume of change in regulations, and say economic pressures, such as inflation, unemployment and exchange rates, make it harder to carry out business with integrity. Geographically, from a list of twelve regions, global legal and compliance respondents cite China (22%), Eastern Europe, including Russia (21%), US and Canada (17%) and Middle East and North Africa (16%) as posing the greatest integrity risks, including compliance and fraud risks, for doing business in the next two years.

- Employee risks: Continuing challenges around misconduct are making it difficult for organizations to drive higher standards of integrity across the business and among third-parties and supply chains. More than one-third (38%) of global respondents say they’d be willing to behave unethically if asked by a manager. Nearly half (47%) of respondents say employees inside their organization pose the greatest integrity risk for the organization over the next two years.

- Operational risks: While 40% cite privacy and security as their greatest operational integrity risks, 53% of global respondents say that employee turnover and employees not understanding policy are the greatest internal threats to organizational standards of integrity.

When conducting risk assessments, it’s important for companies to consider the impact of both internal and external factors on business strategies, commercial activities and employee pressures. It’s also important to understand not only which factors apply but also how and why they apply to link directly to compliance risks and help inform compliance priorities.

What is the root cause of misconduct?

The behavior of potentially compromised employees may be less about being inherently “bad” and more about learned or rationalized behavior.

To better understand what breeds misconduct and how it can thrive, EY teams conducted a deeper analysis of the report data. The results suggest that most organizations can divide their employees into one of three types, based on their willingness to exhibit illegal or unethical behavior:

- “Principled employees” are unwilling to act unethically for personal gain or at the request of a manager.

- “Potentially compromised employees” are willing to act unethically for personal gain or at the request of a manager.

- “Potential enablers” are willing to act unethically at the request of a manager but would not do so for personal gain.

More than half (58%) of employees take a principled approach, indicating that a majority of employees are already inclined to uphold a culture of integrity. However, this leaves a significant remainder of employees within the organization (42%) who are willing to sacrifice integrity under the right conditions. As a result, employees must therefore be properly incentivized and supported when they have the courage to come forward and report wrongdoing, so that misconduct can be appropriately addressed and corrected.

The research shows that potentially compromised employees have a more negative view of their organization’s compliance environment. They are less likely to say their organizations have programs, policies and controls in place to encourage integrity. They’re more likely to say unethical behavior is often tolerated at their organization. Further, they are nearly three times more likely to say that unethical conduct is ignored within their teams, and more than five times more likely to say that unethical conduct is ignored within the supply or distribution chain.

Interestingly, potentially compromised employees are more likely to work for organizations that experienced major integrity events in the past two years, causing more potential reputational harm and incurring more regulatory action.

For potentially compromised employees, breaking with integrity guidelines may be less a question of being hardwired to behave badly and more a question of learned — or rationalized — behavior. They may have the attitude that “if others are doing it, I can get away with it too.” Or “if the company doesn’t care, I would be open to behaving badly if needed or pressured into it.” Fundamentally, it seems that potentially compromised employees can rationalize their behavior because they don’t trust the integrity of the organization.

Similarly, a significant proportion of leaders admit a willingness to behave unethically. Two-thirds (67%) of board members admit they’d be prepared to behave unethically in one or more ways to improve their own career progression or remuneration package (versus only a quarter (25%) of employees).

Further, of those who acknowledge that their organization experienced an integrity incident, 45% attribute the root cause to a lack of appropriate tone from senior leadership or pressure from management.

Tone at the top issues is also reflected in leadership’s willingness to address reported misconduct. While more than half (52%) say they’ve reported misconduct in the last two years (down from 59% in 2022), nearly two-thirds (65%) of those who reported felt under pressure not to report (versus 62% in 2022).

Nearly half (47%) of board members and 40% of senior management also admit that, in the last two years, they’ve seen behavior by other employees that would damage their organization’s reputation if it was known externally and that no action was taken.

Why should employees speak up if leaders don’t act?

Organizations need to create an environment where employees feel psychologically safe to speak up and confident that their concerns will not only be heard, but also acted upon. Whistleblowing, or a “speak- up” culture, is a powerful tool that empowers individuals to speak up against misconduct and unethical behavior, and serves as a crucial safeguard against corruption, fraud and other forms of wrongdoing. According to the Association of Certified Fraud Examiners (ACFE), 43% of all fraud is uncovered through tips by whistleblowers (of those, more than half were employees).

Without an internally supportive environment to speak up when they see wrongdoing, employees may feel better incentivized to report their grievances externally. For example, the Department of Justice’s new Whistleblower Pilot Program in the US, announced in early 2024, aims to incentivize whistleblowers to come forward with information related to corporate misconduct. This program, in addition to other whistleblower programs in the US and globally, may add pressure to an organization’s efforts to encourage employees to report misconduct through internal channels. It’s vital that organizations design and implement internal whistleblower systems that employees trust and all levels of the organization are willing to use without fear of retribution.

Which approach to integrity are you taking?

Organizations typically take one of four approaches to their integrity culture.

Based on the report data and deeper analysis around organizational policies and programs, and how often management speaks about the importance of integrity, EY professionals have learned that, generally, organizations take one of four distinct approaches to their integrity culture:

- Integrity-first: In an integrity-first organization, management speaks frequently about the importance of integrity and puts policies and programs in place to back their words up with actions. In other words, they close the say-do gap. Only 22% of organizations fall into this category, down from 32% in our last report.

- Policy-driven: For 23% of organizations (versus 17% in our previous report), management has taken a policy-driven approach, selecting a range of policies and programs to boost integrity and meet compliance obligations without fully embracing an integrity-first mindset.

- Say-do gap: Executives speak frequently about integrity in organizations that fall into this category. However, they don’t back their words up with actions by implementing policies and programs. Slightly less than half (49%) of organizations take this approach to integrity — roughly the same (47%) as our last report.

- Not a priority: Interestingly, 5% of organizations don’t prioritize the promotion of integrity at all — a statistic that has remained largely static since our last report.

While nearly one-third of organizations were taking an integrity-first approach two years ago, this has dropped to fewer than a quarter based on this year’s findings. Given the increase in organizations that are taking a policy-driven approach, it’s possible that organizations that were previously taking an integrity-first approach believe that, now they have the appropriate policies in place, they no longer need to communicate the importance of integrity as frequently, nor do they see the need to be as vigilant about activating policies as they did before.

These organizations appear to have moved from being on the front foot regarding integrity to allowing integrity to take a back seat while they focus on navigating their business through more volatile economic terrain. Yet it’s in difficult times that an integrity-first approach is most critical. It’s a threshold to which every organization should aspire — in good times and bad times.

Four ways to build a people-centered, integrity-first organization

If the goal is to become an integrity-first organization, the next question leaders may ask is: How do I do that? It starts by putting people at the center of the integrity agenda. People are an organization’s most valued asset and greatest liability when it comes to integrity. As such, they need to be at the heart of the organization’s approach to integrity. This includes implementing supportive frameworks and structures, as well as creating an integrity-first culture that drives positive behaviors and a strong commitment to integrity. Here are four ways GCOs and CCOs can help their companies take to build an integrity-first culture.

1. Lead from the top

The report data demonstrates that integrity can’t be built or sustained on an approach of all talk and no action. Organizations need to focus on preventing and addressing misconduct by starting at the top. GCOs and CCOs should work with leadership to do more than promote ethical behavior — they need to demonstrate it. Additionally, leaders need to not only establish mechanisms for reporting and investigating incidents of misconduct — they must support and follow them. If organizations want to close the say-do gap, leaders need to act with integrity as much as they encourage integrity for those lower down in the organization.

This can be a significant step in creating the supportive environment that employees need to feel comfortable not only behaving with integrity but also intervening or reporting when they see wrongdoing. The more employees see leaders standing up for them and taking concrete action in response to reports of misconduct, without retaliation, the more likely they are to report wrongdoing when they observe it.

2. Design and implement a structure to execute strategy

Structure follows strategy. A strategy without structure can limit the effectiveness of an organization’s integrity program. Organizations need to establish sound governance structures that:

- Align with the organization’s defined roles and responsibilities.

- Establish clear accountability through both key performance indicators (KPIs) and key behavioral indicators (KBIs).

- Break down the silos to allow the free flow of information to those who need it.

- Build trust through transparency.

Further, they need to identify the root cause of wrongdoing, looking beyond simply assigning blame to potentially compromised employees to address systemic challenges.

3. Strengthen a culture of integrity across the organization

Organizations need to recognize that integrity is a team effort. Compliance should not be viewed as a stand-alone support function. Compliance and integrity standards need to be embedded directly into operations and procedures. GCOs and CCOs should work with leadership to incorporate KPIs and KBIs into performance and remuneration across the board. This includes compensation structures that reward employees for demonstrating integrity rather than punishing them for misconduct or noncompliance. In the findings, half of global respondents specifically call out employee and executive compensation structures that punish noncompliance. Metrics should equally focus more on positive reinforcement for behaving with integrity.

4. Boost awareness, training and communication

Respondents say better awareness, training and communication, stronger compliance-related procedures, and improvements to governance and leadership are at the top of their agenda to address integrity risks over the next two years.

Leaders, meanwhile, need to clearly communicate why integrity is important rather than just telling employees what they need to do to comply. Currently, fewer than half (47%) of management teams frequently communicate to their employees the importance of behaving with integrity. Employees are more inclined to comply when they understand the meaning behind what they’re being asked to do.

The value of integrity rests on trust

Integrity is an essential component of trust. Without trust, from employees, customers, suppliers and investors, the future viability of the organization can come under threat. By acknowledging the seriousness of misconduct and taking proactive steps to prevent, detect and address it, companies can build an integrity-first organization that puts people at the center and establishes a robust culture that is supported by unwavering commitment from leadership and on-demand support from employees.

However, for any integrity and compliance program to succeed, companies must start (but not end) with board members and executives, who must set the tone for a culture that doesn’t tolerate misconduct. Words alone won’t inspire loyalty, or even participation. Leaders need to listen, practice what they preach and act against misconduct.

Sadly, there will always be some potentially compromised employees. But, by creating an integrity-first culture that not only encourages but also incentivizes employees to act with integrity, even when no one is looking, organizations can create an environment that truly reflects its belief system and doing the right thing, even in times of adversity and uncertainty.

- Analysis of corporate civil and criminal penalties included in the Violation Tracker (https://violationtracker.goodjobsfirst.org/) and Violation Tracker UK (https://violationtrackeruk.goodjobsfirst.org/) databases, both produced by the Corporate Research Project of Good Jobs First. All penalty amounts were converted to US$ and inflation adjusted to 2023 dollars. This analysis excludes fines of less than US$5,000 (nominal) in the US and includes “cautions” with no dollar amount issued by UK regulators.

- Dyck, Alexander, Morse, Adair, Zingales, Luigi, How pervasive is corporate fraud? , George J. Stigler Center for the Study of the Economy and the State, New Working Paper Series No. #327, January 2023. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4590097#

The EY Global Integrity Report

Previous reports

Download the 2022 EY Global Integrity Report | Tunnel vision or the bigger picture?

Download the 2022 Global Integrity Report: emerging markets perspective | Is your organization upholding its integrity standards?

Download the 2020 EY Global Integrity Report | Is this the moment of truth for corporate integrity?

Download the 2021 EY Global Integrity Report: emerging markets perspective | Is this the moment for emerging markets to prioritize integrity?

Against a backdrop of rapid change, persistent macroeconomic and geopolitical uncertainty, and increased regulatory scrutiny, organizations are finding it more difficult to act with integrity. Yet the findings of the EY Global Integrity Report 2024 suggest it’s not external risks that pose the biggest integrity threat — it’s the organizational culture. The report spells out the urgency to close the gap between what leaders say and how they act, and the steps organizations can take to achieve it.

Related articles

How to balance opportunity and risk in adopting disruptive technologies

Adopting disruptive technologies is a critical challenge for organizations seeking to drive stronger compliance strategy while embracing innovation. Learn more.

About this article

- Connect with us

- Our locations

- Legal and privacy

- Open Facebook profile

- Open X profile

- Open LinkedIn profile

- Open Youtube profile

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

COMMENTS

2023 EY Global Wealth Research Report | EY - Global. Asking the better questions that unlock new answers to the working world's most complex issues. EY helps clients create long-term value for all stakeholders. Enabled by data and technology, our services and solutions provide trust through assurance and help clients transform, grow and operate.

2023 EY Global Wealth Research Report | EY - US. Cybersecurity, strategy, risk, compliance and resilience. Careers in Strategy, M&A and Corporate Finance Consulting. Careers in Climate change and sustainability services. Asking the better questions that unlock new answers to the working world's most complex issues.

T oday's investors are voting with their feet, willing to change advisors and add new relationships, while searching out the products, services and advice they need to make sense of an increasingly complex investing world. That insight is one of the more surprising findings to come from the 2023 EY Global Wealth Research Report. Conducted during a period of exceptional volatility, the ...

A smaller proportion of clients than in the past are looking to move between wealth providers. In 2019, the EY organization found that 32% of clients across the globe planned to move money, down from 40% in 2016. In 2021, just 28% of clients expect to move wealth relationships over the next three years.

2023 EY Global Wealth Management Research Report 3 Global Americas Asia-Pacific EMEIA Wealth managers — like their clients — are facing a complex and uncertain world. Economic and geopolitical instability is heightened, investment strategies are evolving at pace and industry practices are being rapidly transformed by technology.

Nannette Hechler-Fayd'herbe, Chief Investment Officer for the EMEA region and Global Head of Economics & Research at Credit Suisse, said: "While some reversal of the exceptional wealth gains of 2021 is likely in 2022/2023 as several countries face slower growth or even recession, our five-year outlook is for wealth to continue growing ...

Ultimately, our work helps you not just stay competitive, but change investing for the better. Wealth and asset managers are experiencing a time of exponential change. FinTech disruptors continue to shift the rules, newer investors aren't flocking to older channels and cost pressure is relentless. From data and AI, to tech platforms and ...

1 Rising demand, lower loyaltyOne-third of clients plan to switch wealth management providers over the next three years. To stem client attrition and capitalize on this movement, wealth management providers need to understand the who, why and where of client

The recently released EY report, Top 10 resolutions for wealth and asset management success in 2024 ... Mike Lee, global wealth and asset management ... /40 stock/bond portfolio buckled in 2022 ...

lobal Wealth Report 2022 5 Executive summary A record 2021 for household wealth By the end of 2021, global wealth totaled an estimated USD 463.6 trillion, which is an increase of 9.8% versus 2020 and far above the average annual +6.6% recorded since the beginning of the century. Setting aside exchange rate movements, aggregate global wealth grew

Key findings include: Rebounding markets and a brighter outlook lifted 2023 global HNWI wealth by 4.7%,1 and HNWI population numbers increased by 5.1%.2 While growth was seen across all wealth bands, the ultra-HNWI segment (investors with USD 30 million+) enjoyed the most robust recovery in dollar terms. By integrating behavioral finance with ...

T oday's investors are voting with their feet, willing to change advisors and add new relationships, while searching out the products, services and advice they need to make sense of an increasingly complex investing world. That insight is one of the more surprising findings to come from the 2023 EY Global Wealth Research Report. Conducted during a period of exceptional volatility, the ...

Our research identifies 10 underlying challenges that wealth managers must overcome between now and 2030. These challenges ... 2024 EY Global Wealth Management Industry Report: Rethinking the how 7 ... average annual rate of 6.6% between 2000 and 2022, 6 together with rising inequality in both mature and developing markets.

strategy, culture and operations, this year's Global Review also doubles as the EY UNGC communication on progress. 5 EY Global Review 2020 UNGC principle Report section SDG impact Human rights 1. Businesses should support and respect the protection of internationally proclaimed human rights; and Creating long-term value for people

EY Switzerland Sustainability Report 2022. Stefan Rösch-Rütsche. Back About us. Events . Events ... 2023 EY Global Wealth Research Report. As the industry experiences a time of exceptional change, our survey reveals unique client insights and explores industry responses. ... About EY. EY is a global leader in assurance, consulting, strategy ...

There are two particular challenges that companies should confront if they are to close the gap and support a strategy of long-term value creation: • Building a better understanding of the sustainability expectations of investors, and how disclosures can address material ESG issues and earn the trust of stakeholders.

T he 2023 EY Global Wealth Research Report shines a revealing light on the desires and behaviors of wealth management clients around the world. The research covers more than 2,600 clients spanning continents, age groups and levels of wealth. More often than not, it's Millennials that stand out from the crowd.

LONDON, 24 April 2023.The appetite of European 'millennial' investors (those born between 1981 and 1996) to make riskier investments amid market volatility is higher than the generations above them, according to the EY Global Wealth Research Report 2023, as younger investors more actively respond to and are influenced by external market events.

The 2021 EY Global Wealth Research Report survey found that, in APAC, younger generations are more willing to share financial data for the sake of their financial well-being. This means that when they share data, they expect round-the-clock payment services and personalized products. The survey found that 91%3 of millennials are

T he 2023 EY Global Wealth Research Report reveals that nearly half of all wealth management clients worldwide (44%) are planning to change their provider relationships over the next three years - either by adding a new provider (14%), by moving money to another provider (21%) or by switching providers altogether (9%).. Furthermore, clients are planning to move a lot of their money.

T he 2023 EY Global Wealth Research Report reveals that nearly half of all wealth management clients worldwide (44%) are planning to change their provider relationships over the next three years - either by adding a new provider (14%), by moving money to another provider (21%) or by switching providers altogether (9%).. Furthermore, clients are planning to move a lot of their money.

T he EY Global Integrity Report 2024 (pdf) reveals some good news: Almost half (49%) of global respondents think compliance with their organization's standards of integrity has improved in the last two years. This marks an increase of seven percentage points from our EY Global Integrity Report 2022 findings. However, headwinds continue: Nearly four out of 10 (38%) global respondents admit ...