- Global (EN)

- Albania (en)

- Algeria (fr)

- Argentina (es)

- Armenia (en)

- Australia (en)

- Austria (de)

- Austria (en)

- Azerbaijan (en)

- Bahamas (en)

- Bahrain (en)

- Bangladesh (en)

- Barbados (en)

- Belgium (en)

- Belgium (nl)

- Bermuda (en)

- Bosnia and Herzegovina (en)

- Brasil (pt)

- Brazil (en)

- British Virgin Islands (en)

- Bulgaria (en)

- Cambodia (en)

- Cameroon (fr)

- Canada (en)

- Canada (fr)

- Cayman Islands (en)

- Channel Islands (en)

- Colombia (es)

- Costa Rica (es)

- Croatia (en)

- Cyprus (en)

- Czech Republic (cs)

- Czech Republic (en)

- DR Congo (fr)

- Denmark (da)

- Denmark (en)

- Ecuador (es)

- Estonia (en)

- Estonia (et)

- Finland (fi)

- France (fr)

- Georgia (en)

- Germany (de)

- Germany (en)

- Gibraltar (en)

- Greece (el)

- Greece (en)

- Hong Kong SAR (en)

- Hungary (en)

- Hungary (hu)

- Iceland (is)

- Indonesia (en)

- Ireland (en)

- Isle of Man (en)

- Israel (en)

- Ivory Coast (fr)

- Jamaica (en)

- Jordan (en)

- Kazakhstan (en)

- Kazakhstan (kk)

- Kazakhstan (ru)

- Kuwait (en)

- Latvia (en)

- Latvia (lv)

- Lebanon (en)

- Lithuania (en)

- Lithuania (lt)

- Luxembourg (en)

- Macau SAR (en)

- Malaysia (en)

- Mauritius (en)

- Mexico (es)

- Moldova (en)

- Monaco (en)

- Monaco (fr)

- Mongolia (en)

- Montenegro (en)

- Mozambique (en)

- Myanmar (en)

- Namibia (en)

- Netherlands (en)

- Netherlands (nl)

- New Zealand (en)

- Nigeria (en)

- North Macedonia (en)

- Norway (nb)

- Pakistan (en)

- Panama (es)

- Philippines (en)

- Poland (en)

- Poland (pl)

- Portugal (en)

- Portugal (pt)

- Romania (en)

- Romania (ro)

- Saudi Arabia (en)

- Serbia (en)

- Singapore (en)

- Slovakia (en)

- Slovakia (sk)

- Slovenia (en)

- South Africa (en)

- Sri Lanka (en)

- Sweden (sv)

- Switzerland (de)

- Switzerland (en)

- Switzerland (fr)

- Taiwan (en)

- Taiwan (zh)

- Thailand (en)

- Trinidad and Tobago (en)

- Tunisia (en)

- Tunisia (fr)

- Turkey (en)

- Turkey (tr)

- Ukraine (en)

- Ukraine (ru)

- Ukraine (uk)

- United Arab Emirates (en)

- United Kingdom (en)

- United States (en)

- Uruguay (es)

- Uzbekistan (en)

- Uzbekistan (ru)

- Venezuela (es)

- Vietnam (en)

- Vietnam (vi)

- Zambia (en)

- Zimbabwe (en)

- Financial Reporting View

- Women's Leadership

- Corporate Finance

- Board Leadership

- Executive Education

Fresh thinking and actionable insights that address critical issues your organization faces.

- Insights by Industry

- Insights by Topic

KPMG's multi-disciplinary approach and deep, practical industry knowledge help clients meet challenges and respond to opportunities.

- Advisory Services

- Audit Services

- Tax Services

Services to meet your business goals

Technology Alliances

KPMG has market-leading alliances with many of the world's leading software and services vendors.

Helping clients meet their business challenges begins with an in-depth understanding of the industries in which they work. That’s why KPMG LLP established its industry-driven structure. In fact, KPMG LLP was the first of the Big Four firms to organize itself along the same industry lines as clients.

- Our Industries

How We Work

We bring together passionate problem-solvers, innovative technologies, and full-service capabilities to create opportunity with every insight.

- What sets us apart

Careers & Culture

What is culture? Culture is how we do things around here. It is the combination of a predominant mindset, actions (both big and small) that we all commit to every day, and the underlying processes, programs and systems supporting how work gets done.

Relevant Results

Sorry, there are no results matching your search..

- Topic Areas

- Reference Library

Handbook: Financial statement presentation

Handbook | November 2023

Latest edition: In-depth guide on presentation and disclosure requirements, plus considerations under SEC regulations.

Using detailed Q&As and examples, we explain various presentation and general disclosure requirements included in the Codification (i.e. ASC 205 to ASC 280), other broad topics (e.g. related parties under ASC 850 and subsequent events under ASC 855) and SEC regulations. This November 2023 edition incorporates updated guidance and interpretations.

Applicability

- All entities

Relevant dates

- Effective immediately

Key impacts

In the financial statement process, considerable time is devoted to determining what items get recorded and how to account for them, but the critical final mile is determining how they need to appear – i.e. how they are presented and disclosed.

Once the debits and credits have been settled, presentation and disclosure is how that information is conveyed to financial statement users in a transparent, understandable and consistent manner. Disclosure goes ‘behind the numbers’ and is necessary to fully understand the financial statements.

ASC 205 to 280 in the FASB’s Accounting Standards Codification® are dedicated to presentation and disclosure and provide the baseline requirements. Other ASCs address more detailed requirements, specific to certain transactions or industries. For SEC registrants, there is yet more guidance that contains many additional requirements, and which has helped shape practices over the years for all other entities.

In this Handbook, we pull together many of the general requirements and practices to provide you with a fuller picture of how the different financial statements are constructed and how they interact with one another.

Report Contents

- Financial statements: general principles

- Balance sheet

- Income statement

- Comprehensive income

- Notes to the financial statements

- Risks and uncertainties

- Related parties

- Subsequent events

Download the documents:

Financial statement presentation

Executive Summary

Explore more

Handbook: Statement of cash flows

Latest edition: Our comprehensive guide to the statement of cash flows, with Q&As and examples to explain key concepts.

Handbook: Segment reporting

Latest edition: Our comprehensive guide to ASC 280 – with analysis, Q&As and examples.

Handbook: Earnings per share

Latest edition: Our comprehensive guide to EPS, with new and updated interpretive guidance on forward purchase/sale contracts and unit structures.

Meet our team

Subscribe to stay informed

Receive the latest financial reporting and accounting updates with our newsletters and more delivered to your inbox.

Choose your subscription (select all that apply)

By submitting, you agree that KPMG LLP may process any personal information you provide pursuant to KPMG LLP's Privacy Statement .

Accounting Research Online

Access our accounting research website for additional resources for your financial reporting needs.

Thank you for contacting KPMG. We will respond to you as soon as possible.

Contact KPMG

Job seekers

Visit our careers section or search our jobs database.

Use the RFP submission form to detail the services KPMG can help assist you with.

Office locations

International hotline

You can confidentially report concerns to the KPMG International hotline

Press contacts

Do you need to speak with our Press Office? Here's how to get in touch.

- Start Hiring Remote

About Vintti

We're a headhunter agency that connects US businesses with elite LATAM professionals who integrate seamlessly as remote team members — aligned to US time zones, cutting overhead by 70%.

Need to Hire?

We’ll match you with Latin American superstars who work your hours. Quality talent, no time zone troubles. Starting at $9/hour.

I hope you enjoy reading this blog post.

If you want my team to find you amazing talent, click here

Financial Statement Presentation: Structure and Requirements

Written by Santiago Poli on Dec 21, 2023

Preparing financial statements that meet regulatory requirements can be an overwhelming task for many organizations.

This article provides a comprehensive guide to the key components, structure, and presentation standards for financial statements to ensure proper compliance and disclosure.

We will explore the five main financial statements, breakdown the required elements of each statement, review relevant accounting standards from GAAP and IFRS, and provide practical examples and templates to guide your financial statement preparation. By following the recommendations outlined here, you can create accurate, compliant financial statements tailored to your specific reporting needs.

Introduction to Financial Statement Presentation

Financial statements are formal reports that summarize a company's financial performance over a period of time. They communicate key information to internal and external stakeholders to facilitate decision-making. Proper financial statement presentation is vital for businesses to effectively convey their financial position.

This section will provide an overview of financial statement presentation, including its purpose, key components, and regulatory requirements. It will introduce the 5 main components of financial statements and discuss how proper presentation is vital for businesses.

Understanding the 5 Components of Financial Statements

Financial statements generally contain 5 key components:

- Income Statement - Reports revenue, expenses, and profit/loss over a period of time

- Balance Sheet - Snapshot of assets, liabilities, and equity on a certain date

- Cash Flow Statement - Depicts inflows and outflows of cash

- Statement of Stockholders' Equity - Shows changes in equity accounts

- Notes to Financial Statements - Additional disclosures and details

These 5 reports work together to provide a comprehensive view of a company's finances. Proper categorization and presentation of each component is necessary for stakeholders to accurately interpret performance.

Significance of Financial Statement Presentation

Financial statement presentation standards exist to:

- Communicate Performance - Well-structured reports allow readers to clearly see profitability, liquidity, leverage, etc.

- Meet Regulatory Requirements - Public companies must follow strict presentation rules.

- Facilitate Decision-Making - With organized information, internal and external decisions can be made effectively.

Following presentation guidelines ensures transparency and enables financial analysis .

Regulatory Framework: ASC 205 and IAS 1

In the US, the FASB's ASC 205 establishes presentation principles for financial statements. Similarly, the IASB's IAS 1 outlines international standards. These regulations dictate:

- Statement ordering and content

- Classification and aggregation

- Disclosures

Understanding the regulatory presentation framework is key for proper financial reporting .

Proper financial statement presentation acts as the foundation for communicating performance. By classifying information correctly and meeting presentation standards, businesses can clearly convey their financial position.

What are the requirements for fair presentation of financial statements?

Fair presentation of financial statements requires adherence to accounting standards and a faithful representation of the company's financial position. Some key requirements include:

Compliance with Applicable Accounting Standards

Financial statements must comply with the applicable accounting standards framework, such as:

- US GAAP - Generally Accepted Accounting Principles in the United States

- IFRS - International Financial Reporting Standards

This ensures standardized reporting across companies.

Faithful Representation

Financial statements should faithfully represent the economic reality of transactions and events. Information should be complete, neutral, and free from material error.

Understandability

Financial information should be presented clearly and concisely. Companies should provide adequate disclosures and explanation of accounting policies , estimates, and judgements.

Information in financial statements should be relevant to the decision-making needs of users. Only include information that is capable of making a difference in decisions.

Materiality

Companies must provide all material information - those that can reasonably influence users' decisions. Immaterial information can be excluded.

Comparability

Financial reporting should allow users to identify similarities and differences across reporting periods and between entities. Consistent presentation and reporting facilitates comparison.

Following accounting rules and standards, as well as providing relevant, faithful, and clear information is key to achieving fair presentation of financial statements.

How do you present financial statements in a presentation?

When presenting financial statements, it is important to focus on communicating the key information clearly and effectively to your audience. Here are some tips:

Keep it simple

Avoid using complex financial jargon and acronyms that may confuse your audience. Present key figures, trends, and takeaways in easy-to-understand language. Use examples if needed to illustrate your points.

Use visuals

Visual aids like charts, graphs, and tables can help reinforce numbers and make financial data more digestible. Choose clear, uncluttered designs over flashy graphics. Emphasize key metrics and trends.

Tell a story

Structure your presentation to take the audience on a logical journey. Explain the meaning behind the numbers, and how they relate to broader company strategy and performance. Draw connections between financial statements.

Tailor to your audience

Understand what financial information your audience cares about most, and focus on highlighting the relevant key performance indicators that align to their interests or concerns.

Practice effective delivery

Speak slowly and clearly. Maintain eye contact and gauge audience reaction. Be prepared to answer questions on the details behind your summary figures.

Following these tips can lead to financial presentations that clearly communicate meaning and impact.

How should financial statements be presented?

Financial statements should be presented in a clear, structured format that complies with accounting standards and principles .

General Presentation Guidelines

- Financial statements typically include a balance sheet, income statement, statement of cash flows, and statement of stockholders' equity. Notes and disclosures provide important details.

- Assets are generally presented from most liquid to least liquid, while liabilities are presented from short-term to long-term.

- Positive numbers indicate assets and revenues, while negative numbers signify liabilities, equity, expenses or losses.

- Subtotals and totals should be clearly labeled for each financial statement category or section to improve readability.

Disclosure Requirements

Certain disclosures are required by accounting standards like GAAP or IFRS in the footnotes and statement notes. These include:

Accounting policies used

Details on material asset, liability and equity accounts

Segment and geographical reporting

Commitments and contingencies

Disclosures should provide clarity on any aspects of the financial statements that may be unclear or require further explanation.

Following standard presentation guidelines and properly disclosing important details leads to higher quality, more transparent and understandable financial statements.

What are the requirements for financial statements?

Financial statements need to adhere to certain basic requirements to accurately reflect a company's financial position. These include:

Fair Presentation

Financial statements must fairly present the financial position, performance, and cash flows of an entity. This requires compliance with accounting standards as well as providing adequate disclosures and descriptions to give users an accurate picture of the company's finances.

Going Concern

Financial statements are prepared under the assumption that the entity will continue operating in the foreseeable future. If there are doubts about the company's ability to do so, appropriate disclosures must be made.

Accrual Basis

Financial statements are prepared using the accrual basis of accounting, meaning that economic events are recognized when they occur, not when cash is exchanged. This better matches revenues and expenses to the period in which they were incurred.

Materiality and Aggregation

Information is material if omitting or misstating it could influence decisions made by users of the financial statements. Immaterial items can be aggregated to avoid cluttering statements.

No Offsetting

Assets and liabilities, and income and expenses, cannot be offset against each other unless specifically permitted by the accounting standards. Offsetting obscures useful information.

In summary, financial statements must provide a fair, going concern view of the entity's finances on an accrual basis. They should include all material information without aggregation or offsetting. Most companies must prepare financial statements at least annually and include comparative info from prior periods. Consistency in presentation over time is also key.

sbb-itb-beb59a9

Structuring financial statements: a detailed look.

Financial statements are structured reports that summarize a company's financial position and performance over a period of time. The five main financial statements are:

Income Statement Breakdown

The income statement shows a company's revenues, expenses, and net income over a period of time, usually a quarter or year. Key components include:

- Revenue - Money earned from the company's operations, products, or services

- Cost of Goods Sold (COGS) - Direct expenses related to providing products/services

- Operating Expenses - Indirect expenses like marketing, R&D, administration

- Operating Income - Revenue minus COGS and operating expenses

- Other Income/Expenses - Taxes, interest earned/paid

- Net Income - The "bottom line" profit or loss after subtracting all expenses

The income statement shows whether a company made a profit or loss during the period.

Analyzing the Balance Sheet

The balance sheet is a snapshot of a company's financial position at a point in time. Key components include:

Assets - Resources owned by the company with economic value. Common asset types:

- Current Assets - Cash, accounts receivable, inventory

- Fixed Assets - Property, plants, equipment

- Intangible Assets - Patents, trademarks, goodwill

Liabilities - Debts and obligations owed by the company:

- Current Liabilities - Due within 12 months, e.g. accounts payable

- Long-Term Debt - Due after 12 months, e.g. bonds payable

Shareholders' Equity - Value that would be returned to shareholders if assets were liquidated and debts paid off. Includes:

- Paid-in Capital - Amounts invested by shareholders

- Retained Earnings - Company profits not paid out as dividends

The balance sheet shows the company's financial health and liquidity position.

Cash Flow Statement Categorization

The cash flow statement tracks the actual cash coming into and going out of the business. Cash flows are categorized into:

- Operating Activities - Core business operations, e.g. cash received from customers

- Investing Activities - Investments in capital expenditures, securities, etc.

- Financing Activities - Cash from financing sources like loans and equity issuances

Analyzing the sources and uses of cash flow indicates whether the company is generating enough cash to sustain itself.

Presentation of the Statement of Retained Earnings

The statement of retained earnings summarizes changes in retained earnings over a period. It starts with the prior period's retained earnings, adds net income earned during the current period, and subtracts any dividends paid to shareholders.

The ending retained earnings balance is shown on the balance sheet. Tracking changes helps assess how much of the company's profits are being reinvested vs. paid out to shareholders.

Components of the Statement of Shareholders' Equity

The statement of shareholders' equity summarizes changes in the equity accounts over a period. Key components include:

- Paid-in Capital - Additional investments by shareholders

- Treasury Stock - Company repurchases of outstanding shares

- Retained Earnings - Company profits not paid as dividends

- Accumulated Other Comprehensive Income - Certain income statement items

This statement reconciles the beginning and ending shareholders' equity balances on the balance sheet.

Financial Statement Presentation Standards and Requirements

Financial statement presentation is crucial for effectively communicating a company's financial position and performance to stakeholders. Companies must follow strict presentation standards and requirements outlined by accounting regulations like US GAAP and IFRS.

Adhering to US GAAP Financial Statements Format

The FASB Accounting Standards Codification (ASC) Topic 205 summarizes the core presentation requirements for US GAAP financial statements. Key elements include:

- Classifying the balance sheet into current and noncurrent assets and liabilities

- Presenting expenses by function or nature in the income statement

- Including a statement of cash flows and statement of changes in equity

- Disclosing relevant information in footnotes

Companies should reference ASC 205 and related regulations when preparing financials to ensure proper US GAAP format and disclosure.

Compliance with IFRS and IAS 1 Presentation Standards

International Financial Reporting Standards (IFRS) share similarities with US GAAP but have key differences in presentation under IAS 1 (PDF here). These include:

- Stricter requirements about items presented on the balance sheet and income statement

- Different classifications of expenses and equity

- More flexibility in formatting statements

It is critical for multinational companies to understand both US GAAP and IFRS presentation standards.

Navigating SEC Disclosure Requirements

Public companies in the US must also follow Securities and Exchange Commission (SEC) disclosure rules that impact financial statement presentation. Examples include:

- Segment reporting disclosures about products, services, and geographic areas

- Related party transaction footnotes

- Disclosures of risk factors and uncertainties

See PwC's guide for best practices on SEC disclosures.

Avoiding Common Financial Statement Presentation Pitfalls

Some common financial statement presentation mistakes include:

- Inconsistent classification of expenses across periods

- Netting accounts that should be presented gross

- Failing to properly disclose uncertainties or contingencies

Companies should reference EY's presentation guide and have external audits done to identify areas for improvement.

Exploring Disclosures and Supplementary Information

This section will examine common supplementary financial information and disclosures provided alongside or within financial statements, and their significance in providing a complete financial picture.

Detailing Accounting Policies and Disclosures

Financial statements must include significant accounting policies as a footnote, summarizing principles related to revenue recognition , depreciation methods, valuation of inventories, investments, etc. These disclosures ensure transparency on assumptions and estimates made in preparing the statements.

For example, a retail company may disclose:

- Revenue is recognized at the point of sale when goods are sold to customers.

- Inventory is valued using the FIFO method.

- Fixed assets are depreciated over useful lives of 3-10 years using the straight-line method.

Other vital disclosures provide details on litigation risks, contractual obligations, segment performance, related party transactions , pension plan assets and obligations, etc. These offer context for assessing the company's financial health.

Insights from Management's Discussion and Analysis (MD&A)

The MD&A section discusses the company's financial performance, changes in financial position, and outlook. It analyzes trends in liquidity, capital resources, operations, industry conditions, and other factors impacting the business.

For instance, the MD&A may attribute a revenue decline to specific economic or competitive challenges. Or it may link an increase in capital expenditures to investments in new production facilities. This qualitative perspective supplements the quantitative data in financial statements.

Financial Ratio Analysis and Benchmarks

Many companies include key financial ratios like return on equity , profit margin, asset turnover, debt-to-equity alongside industry benchmarks.

For example, an industrial manufacturer may compare its gross margin percentage, inventory turnover ratio, and days sales outstanding ratio to industry averages. This allows contextual assessment of financial performance.

Benchmarking also assists lenders and investors in comparing companies within an industry when making investment decisions.

Types of Disclosures in Financial Statements

Common disclosures in financial statements include:

- Contingencies: Litigation, environmental liabilities, warranties

- Related parties: Transactions with affiliated entities

- Risks: Interest rate, currency, credit risk exposures

- Subsequent events: Significant events occurring after fiscal yearend

- Uncertainties: Potential asset impairments, variability in estimates

- Segment details: Revenue, assets, profitability by product line or geography

Such disclosures increase transparency on uncertainties inherent in financial reporting and assumptions made by management. They provide vital perspective for financial statement users and must be presented appropriately as per accounting standards.

Practical Examples and Guides for Financial Statement Presentation

This section provides practical financial statement presentation examples and explores resources like the PwC and EY financial statement presentation guides.

Financial Statement Presentation Example

Here is an example of a basic financial statement presentation for a fictional company:

Income Statement

- Revenue: $100,000

- Cost of Goods Sold: $60,000

- Gross Profit: $40,000

- Operating Expenses: $20,000

- Operating Income: $20,000

- Interest Expense: $2,000

- Pretax Income: $18,000

- Income Tax: $5,000

- Net Income: $13,000

Balance Sheet

- Cash: $10,000

- Accounts Receivable: $5,000

- Inventory: $15,000

- Total Assets: $30,000

- Liabilities

- Accounts Payable: $4,000

- Total Liabilities: $4,000

- Shareholders' Equity

- Common Stock: $10,000

- Retained Earnings: $16,000

- Total Liabilities and Equity: $30,000

Cash Flow Statement

- Operating Activities

- Changes in Working Capital: $5,000

- Net Cash from Operations: $18,000

- Investing Activities

- Equipment Purchases: -$3,000

- Financing Activities

- Dividends Paid: -$5,000

- Change in Cash: $10,000

This illustrates the core components and layout of financial statements. Companies provide further disclosures and details in the footnotes.

Leveraging the PwC Financial Statement Presentation Guide PDF

The PwC financial statement presentation guide provides a comprehensive overview of financial statement presentation requirements under IFRS . Key aspects covered include:

- General presentation principles

- Statement of financial position structure

- Income statement layout and disclosures

- Standards for the statement of changes in equity

- Cash flow statement preparation

The guide serves as an authoritative reference for ensuring financial statements adhere to the latest standards and presentation best practices. Companies can leverage the guide when structuring their financial reports to improve quality, transparency, and compliance.

Utilizing the EY Financial Statement Presentation Guide

The EY financial statement presentation guide delivers insights into effectively presenting financial information to stakeholders. Areas covered include:

- Optimizing the balance sheet structure

- Enhancing the clarity of the income statement

- Improving cash flow statement usefulness through classification

- Making critical judgment calls on presentation

- Providing high quality disclosures

By consulting the guide, finance teams can apply EY's presentation best practices to their financial reporting processes. This helps improve the understandability and decision-usefulness of statements for investors and regulators.

Conclusion: Mastering Financial Statement Presentation

Proper financial statement presentation is critical for communicating accurate and transparent information to stakeholders. As discussed, key requirements per GAAP and IFRS standards include:

- Presenting comparative financial statements covering at least two reporting periods

- Clearly labeling each financial statement and its components

- Disclosing relevant information in the notes to assist in interpretation

- Following formatting and component ordering conventions

By mastering guidelines around statement structure, organizations build trust and enable sound decision-making. Key lessons for financial professionals include:

- Understand regulatory presentation standards based on jurisdiction

- Analyze comparative trends and performance over time

- Assess which disclosures are material to the reader

- Format statements consistently across periods

- Focus on transparency through clear communication

Meeting presentation requirements takes diligence, but pays dividends in stakeholder confidence. Financial leaders should continue honing their expertise in this critical discipline.

Related posts

- Delving into IFRS Standards: A Comprehensive Review

- Interim Financial Reporting: GAAP Requirements

- Understanding Consolidated Financial Statements

- Balance Sheet vs Income Statement

Looking to hire? We'll help you find the best talent.

See how we can help you find a perfect match in only 20 days. Interviewing candidates is free!

Looking for help? we help you hire the best talent

You can secure high-quality South American for around $9,000 USD per year. Interviewing candidates is completely free ofcharge.

Related articles

10 Tips to Prepare for Tax Season

To help you prepare for the upcoming tax season, here are 10 tips that can make your work more efficient, effective, and enjoyable.

The Full Overview of Offshore Accountants: Top Countries for Outsourcing

CPA firms resolve their staffing need with offshore accountants. South America vs Asia. Nearshore vs Offshore Competitive Salary, Scalability, and Top Skills.

Best 5 Tools for Remote Onboarding

Remote onboarding for offshore accounting teams is a strategic move that offers numerous benefits to accounting and finance firms.

Find the talent you need to grow your business

You can secure high-quality South American talent in just 20 days and for around $9,000 USD per year.

IFRScommunity.com

IFRS Forums and IFRS Knowledge Base

Presentation of Financial Statements (IAS 1)

Last updated: 17 May 2024

IAS 1 serves as the main standard that outlines the general requirements for presenting financial statements. It is applicable to ‘general purpose financial statements’, which are designed to meet the informational needs of users who cannot demand customised reports from an entity. Documents like management commentary or sustainability reports, which are often included in annual reports, fall outside the scope of IFRS, as indicated in IAS 1.13-14. Similarly, financial statements submitted to a court registry are not considered general purpose financial statements (see IAS 1.BC11-13).

The standard primarily focuses on annual financial statements, but its guidelines in IAS 1.15-35 also extend to interim financial reports (IAS 1.4). These guidelines address key elements such as fair presentation, compliance with IFRS, the going concern principle, the accrual basis of accounting, offsetting, materiality, and aggregation. For comprehensive guidance on interim reporting, please refer to IAS 34 .

Note that IAS 1 will be superseded by the upcoming IFRS 18 Presentation and Disclosure in Financial Statements .

Now, let’s explore the general requirements for presenting financial statements in greater detail.

Financial statements

Components of a complete set of financial statements.

Paragraph IAS 1.10 outlines the elements that make up a complete set of financial statements. Companies have the flexibility to use different titles for these documents, but each statement must be presented with equal prominence (IAS 1.11). The terminology used in IAS 1 is tailored for profit-oriented entities. However, not-for-profit organisations or entities without equity (as defined in IAS 32), may use alternative terminology for specific items in their financial statements (IAS 1.5-6).

Are you tired of the constant stream of IFRS updates? I know it's tough! That's why I created Reporting Period – a once-a-month summary for professional accountants. It consolidates all essential IFRS developments and Big 4 insights into one readable email. I personally curate every issue to ensure it's packed with the most relevant information, delivered straight to your inbox. It's free, with no spam, and if it turns out not to be right for you, you can unsubscribe with just one click.

Compliance with IFRS

Financial statements must include an explicit and unreserved statement of compliance with IFRS in the accompanying notes. This statement is only valid if the entity adheres to all the requirements of every IFRS standard (IAS 1.16). In many jurisdictions, such as the European Union, laws mandate compliance with a locally adopted version of IFRS.

IAS 1 does consider extremely rare situations where an entity might diverge from a specific IFRS requirement. Such a departure is permissible only if it prevents the presentation of misleading information that would conflict with the objectives of general-purpose financial reporting (IAS 1.20-22). Alternatively, entities can disclose the impact of such a departure in the notes, explaining how the statements would appear if the exception were made (IAS 1.23).

Identification of financial statements

The guidelines for identifying financial statements outlined in IAS 1.49-53 are straightforward and rarely cause issues in practice.

Going concern

The ‘going concern’ principle is a cornerstone of IFRS and other major GAAP. It assumes that an entity will continue to operate for the foreseeable future (at least 12 months). IAS 1 mandates management to assess whether the entity is a ‘going concern’. Should there be any material uncertainties regarding the entity’s future, these must be disclosed (IAS 1.25-26). IFRSs do not provide specific accounting principles for entities that are not going concerns, other than requiring disclosure of the accounting policies used. One of the possible approaches is to measure all assets and liabilities using their liquidation value.

See also this educational material at IFRS.org.

Materiality and aggregation

IAS 1.29-31 emphasise the importance of materiality in preparing user-friendly financial statements. While IFRS mandates numerous disclosures, entities should only include information that is material. This concept should be at the forefront when preparing financial statements, as reminders about materiality are seldom provided in other IFRS standards or publications.

Generally, entities should not offset assets against liabilities or income against expenses unless a specific IFRS standard allows or requires it. IAS 1.32-35 offer guidance on what can and cannot be offset. Offsetting of financial instruments is discussed further in IAS 32 .

Frequency of reporting

Entities are required to present a complete set of financial statements at least annually (IAS 1.36). However, some Public Interest Entities (PIEs) may be obliged to release financial statements more frequently, depending on local regulations. However, these are typically interim financial statements compiled under IAS 34 .

IAS 1 also allows for a 52-week reporting period instead of a calendar year (IAS 1.37). This excerpt from Tesco’s annual report serves to demonstrate this point, showing that the group uses 52-week periods for their financial year, even when some subsidiaries operate on a calendar-year basis:

If an entity changes its reporting period, it must clearly disclose this modification and provide the rationale for the change (IAS 1.36). It is advisable to include an explanatory note with comparative data that aligns with the new reporting period for clarity.

Comparative information

As a general guideline, entities should present comparative data for the prior period alongside all amounts reported for the current period, even when specific guidelines in a given IFRS do not require it. However, there’s no obligation to include narrative or descriptive information about the preceding period if it isn’t pertinent for understanding the current period (IAS 1.38).

If an entity opts to provide comparative data for more than the immediately preceding period, this additional information can be included in selected primary financial statements only. However, these additional comparative periods should also be detailed in the relevant accompanying notes (IAS 1.38C-38D).

IAS 1.40A-46 outlines how to present the statement of financial position when there are changes in accounting policies, retrospective restatements, or reclassifications. This entails producing a ‘third balance sheet’ at the start of the preceding period (which may differ from the earliest comparative period, if more than one is presented). Key points to note are:

- The third balance sheet is required only if there’s a material impact on the opening balance of the preceding period (IAS 1.40A(b)).

- If a third balance sheet is included, there’s no requirement to add a corresponding third column in the notes, although this could be useful where numbers have been altered by the change (IAS 1.40C).

- Interim financial statements do not require a third balance sheet (IAS 1.BC33).

IAS 8 also requires comprehensive disclosures concerning changes in accounting policies and corrections of errors .

Statement of financial position

IAS 1.54 enumerates the line items that must, at a minimum, appear in the statement of financial position. Entities should note that separate lines are not required for immaterial items (IAS 1.31). Additional line items can be added for entity-specific or industry-specific matters. IAS 1 permits the inclusion of subtotals, provided the criteria set out in IAS 1.55A are met.

Additional disclosure requirements are set out in IAS 1.77-80A. Of particular interest are the requirements pertaining to equity (IAS 1.79), which begin with the number of shares and extend to include details such as ‘rights, preferences, and restrictions relating to share capital, including restrictions on the distribution of dividends and the repayment of capital.’ While these kinds of limitations are common across various legal jurisdictions (for example, not all retained earnings can be distributed as dividends), many companies neglect to disclose such limitations in their financial statements.

For guidance on classifying assets and liabilities as either current or non-current, please refer to the separate page dedicated to this topic.

Statement of profit or loss and other comprehensive income

IAS 1 provides two methods for presenting profit or loss (P/L) and other comprehensive income (OCI). Entities can either combine both P/L and OCI into a single statement or present them in separate statements (IAS 1.81A-B). Additionally, the P/L and total comprehensive income for a given period should be allocated between the owners of the parent company and non-controlling interests (IAS 1.81B).

Minimum contents in P/L and OCI

IAS 1.82-82A specifies the minimum items that must appear in the P/L and OCI statements. These items are required only if they materially impact the financial statements (IAS 1.31).

Entities are permitted to add subtotals to the P/L statement if they meet the criteria specified in IAS 1.85A. Operating income is often the most commonly used subtotal in P/L. This practice may be attributed to the 1997 version of IAS 1, which mandated the inclusion of this subtotal—although this is no longer the case. IAS 1.BC56 clarifies that an operating profit subtotal should not exclude items commonly considered operational, such as inventory write-downs, restructuring costs, or depreciation/amortisation expenses.

Profit or loss (P/L)

All items of income and expense must be recognised in P/L (or OCI). This means that no income or expenses should be recognised directly in the statement of changes in equity, unless another IFRS specifically mandates it (IAS 1.88). Direct recognition in equity may also result from intra-group transactions . IAS 1.97-98 require separate disclosure of material items of income and expense, either directly in the income statement or in the notes.

Expenses in P/L can be presented in one of two ways (IAS 1.99-105):

- By their nature (e.g., depreciation, employee benefits); or

- By their function within the entity (e.g., cost of sales, distribution costs, administrative expenses).

When opting for the latter, entities must provide additional details on the nature of the expenses in the accompanying notes (IAS 1.104).

Other comprehensive income (OCI)

OCI encompasses income and expenses that other IFRS specifically exclude from P/L. There is no conceptual basis for deciding which items should appear in OCI rather than in P/L. Most companies present P/L and OCI as separate statements, partly because OCI is generally overlooked by investors and those outside of accounting and financial reporting circles. The concern is that combining the two could reduce net profit to merely a subtotal within total comprehensive income.

All elements that constitute OCI are specifically outlined in IAS 1.7, as part of its definitions.

Reclassification adjustments

A reclassification adjustment refers to the amount reclassified to P/L in the current period that was recognised in OCI in the current or previous periods (IAS 1.7). All items in OCI must be grouped into one of two categories: those that will or will not be subsequently reclassified to P/L (IAS 1.82A). Reclassification adjustments must be disclosed either within the OCI statement or in the accompanying notes (IAS 1.92-96).

To illustrate, foreign exchange differences arising on translation of foreign operations and gains or losses from certain cash flow hedges are examples of items that will be reclassified to P/L. In contrast, remeasurement gains and losses on defined benefit employee plans or revaluation gains on properties will not be reclassified to P/L.

The practice of transferring items from OCI to P/L, commonly known as ‘recycling’, lacks a concrete conceptual basis and the criteria for allowing such transfers in IFRS are often considered arbitrary.

Tax effects

OCI items can be presented either net of tax effects or before tax, with the overall tax impact disclosed separately. In either case, entities must specify the tax amount related to each item in OCI, including any reclassification adjustments (IAS 1.90-91). Interestingly, there is no such requirement to disclose tax effects for individual items in the income statement.

Statement of changes in equity

IAS 1.106 outlines the minimum line items that must be included in the statement of changes in equity. Subsequent paragraphs specify the disclosure requirements, which can be addressed either within the statement itself or in the accompanying notes. It’s crucial to note that changes in equity during a reporting period can arise either from income and expense items or from transactions involving owners acting in their capacity as owners (IAS 1.109). This means that entities cannot adjust equity directly based on changes in assets or liabilities unless these adjustments result from transactions with owners, such as capital contributions or dividend payments, or are otherwise mandated by other IFRSs.

Statement of cash flows

The statement of cash flows is governed by IAS 7 .

- Explanatory notes

Structure of explanatory notes

The structure for explanatory notes is detailed in IAS 1.112-116. In practice, there are several commonly adopted approaches to organising these notes:

Approach #1:

- Primary financial statements (P/L, OCI, etc.)

- Statement of compliance and basis of preparation

- Accounting policies

Approach #1 is logically coherent, as understanding accounting policies is crucial before delving into the financial data. However, in reality, few people read the accounting policies in their entirety. Consequently, users often have to navigate past several pages of accounting policies to reach the explanatory notes.

Approach #2:

- Primary financial statements (P/L, OCI, etc)

In Approach #2, accounting policies are treated as an appendix and positioned at the end of the financial statements. The advantage here is that all numerical data is clustered together, uninterrupted by extensive descriptions of accounting policies.

Approach #3:

- Explanatory notes integrated with relevant accounting policies

Approach #3 pairs accounting policies directly with the associated explanatory notes. For example, accounting policies relating to inventory would appear alongside the explanatory note that breaks down inventory components.

Management of capital

IAS 1.134-136 outline the disclosures related to capital management. These provisions apply to all entities, whether or not they are subject to external capital requirements. An important note here is that entities are not obligated to disclose specific values or ratios concerning capital objectives or requirements.

IAS 1.137 mandates disclosure of dividends proposed or declared before the financial statements were authorised for issue but not recognised as a distribution to owners during the period. Furthermore, entities are required to disclose the amount of any cumulative preference dividends not recognised.

Disclosure of accounting policies

IAS 1 specifies the requirements for disclosing accounting policy information which are discussed here .

Disclosing judgements and sources of estimation uncertainty

IAS 1 mandates disclosing judgements and sources of estimation uncertainty .

Other disclosures

Additional miscellaneous disclosure requirements are detailed in paragraphs IAS 1.138.

IFRS 18 Presentation and Disclosure in Financial Statements

On 9 April 2024, the IASB issued IFRS 18 Presentation and Disclosure in Financial Statements , which replaces IAS 1 and amends IAS 7. This new standard will be effective from 2027 with early application permitted.

Here are the key changes under IFRS 18:

- Two new subtotals have been added to the income statement: ‘Operating Profit’ and ‘Profit Before Financing and Income Taxes’. This change requires companies to categorise income and expenses into operating, investing, and financing activities.

- A new requirement mandates the reconciliation of non-GAAP measures with IFRS-specified subtotals, but this only applies to P/L measures such as adjusted profit. Other metrics like free/organic cash flow or net debt are not included.

- The statement of cash flows will start with operating profit for the indirect method, and the classification of cash flows related to interest and dividends has been standardised. Typically, dividends and interest paid will fall under financing activities, while those received will be recorded under investing activities.

While many IAS 1 provisions remain under IFRS 18, others, including the basis of financial statement preparation and disclosure of accounting policies, have moved to IAS 8, which will be retitled Basis of Preparation of Financial Statements . For further insights, see the IASB Project Summary .

© 2018-2024 Marek Muc

The information provided on this website is for general information and educational purposes only and should not be used as a substitute for professional advice. Use at your own risk. Excerpts from IFRS Standards come from the Official Journal of the European Union (© European Union, https://eur-lex.europa.eu). You can access full versions of IFRS Standards at shop.ifrs.org. IFRScommunity.com is an independent website and it is not affiliated with, endorsed by, or in any other way associated with the IFRS Foundation. For official information concerning IFRS Standards, visit IFRS.org.

Questions or comments? Join our Forums

IAS 1 Presentation of Financial Statements: Summary

IAS 1 Presentation of Financial Statements represents a basis of the whole IFRS reporting, as it sets overall requirements for the presentation of financial statements, guidelines for their structure and minimum requirements for their content.

Financial Statements

Purpose of the financial statements is to provide information about the financial position, financial performance and cash flows of an entity that is useful to a wide range of users in making economic decisions.

The complete set of financial statements compliant with IFRS comprises 5 elements:

- a statement of financial position as at the end of the period

- a statement of comprehensive income for the period

- a statement of changes in equity for the period

- a statement of cash flows for the period

- notes containing a summary of significant accounting policies and other explanatory information.

If some accounting policy is applied retrospectively, or some retrospective restatements or reclassifications were made, then also a statement of financial position as at the beginning of the earliest comparative period shall be presented.

IAS 1 explains the general features of financial statements, such as fair presentation and compliance with IFRS , going concern, accrual basis of accounting, materiality and aggregation, offsetting, frequency of reporting, comparative information and consistency of presentation.

Structure and Content

IAS 1 requires identification of the financial statements and distinguishing them from other information in the same published document.

Every element of the financial statements shall contain the name of the reporting entity, the information whether the financial statements are of an individual or of a group, the date of the reporting entity and period covered, the presentation currency and the level of rounding (thousands, millions…).

IAS 1 lists the minimum content to be presented in the financial statements, except for the statement of cash flows (subject to IAS 7). So let’s look at it in a detail.

Statement of Financial Position

Before significant amendments of IAS 1, this statement was simply called “balance sheet”, however, it was renamed.

IAS 1 requires presentation of classified statement of financial position where current assets or liabilities are separated from non-current assets or liabilities. Basically, the asset or liability is current when it is expected to be recovered or settled within 12 months after the reporting period.

With regard to a minimum content, the following line items shall be presented:

| ASSETS | EQUITY AND LIABILITIES |

|---|---|

| Property, plant and equipment | Issued capital and reserves attributable to owners of the parent |

| Investment property | |

| Intangible assets | Non-controlling interests |

| Financial assets | Financial Liabilities |

| Investments accounted for using equity method | Provisions |

| Biological assets | |

| Inventories | |

| Trade and other receivables | Trade and other payables |

| Cash and cash equivalents | |

| Totals of assets in accordance with IFRS 5 Non-current assets Held for Sale and Discontinued Operations | Totals of liabilities in accordance with IFRS 5 Non-current assets Held for Sale and Discontinued Operations |

| Current tax assets | Current tax liabilities |

| Deferred tax assets | Deferred tax liabilities |

Further subclassifications of the line items shall be disclosed either directly in the statement of financial position or in the notes, such as disaggregation of property, plant and equipment into classes, and similar. Also, certain information related to the share capital, reserves and a few others shall be included in the statement of financial position, the statement of changes in equity or in the notes.

IAS 1 does NOT prescribe the precise format of the statement of financial position. Instead, several formats are acceptable if they fulfill all requirements outlined above.

Statement of Comprehensive Income

The statement of comprehensive income has 2 basic elements:

- Profit or loss for the period : here, all items of income and expenses must be recognized.

- Other comprehensive income : items recognized directly to equity or reserves, such as changes in revaluation surplus, gains or losses from subsequent measurement of available-for-sale financial assets, etc.

As a minimum , the statement of comprehensive income must contain the following items:

| PROFIT OR LOSS |

|---|

| Revenue |

| Gains and losses arising from the derecognition of financial assets at amortized cost |

| Finance costs |

| Share of the profit or loss of associates and joint ventures accounted for using the equity method |

| Tax expense |

| Post-tax profit/gain or loss of operations or assets in accordance with IFRS 5 (Non-current assets Held for Sale and Discontinued Operations) |

| Profit or loss |

| OTHER COMPREHENSIVE INCOME |

| Each component of other comprehensive income classified by nature |

| Share of the other comprehensive income of associates and joint ventures accounted for using equity method |

| Total comprehensive income |

As opposed to US GAAP , IAS 1 prohibits to report any transaction or item as extraordinary items.

Profit or loss for the period, as well as total comprehensive income shall be both presented in allocation:

- attributable to non-controlling interests and

- attributable to owners of the parent.

The entity might choose to classify expenses recognized in profit or loss for the period by their nature or by their function.

IAS 1 requires disclosure of certain items separately , either in the statement of comprehensive income, or in the notes. These items are as follows: write-downs of inventories and property, plant and equipment, their reversals, restructuring of activities and reversals of related provisions, disposals of property, plant and equipment, disposals of investments, discontinuing operations, litigation settlements and other reversals of provisions.

Statement of Changes in Equity

As a minimum , the statement of changes in equity must contain the following items:

- total comprehensive income for the period, showing separately amounts attributable to owners of the parent and to non-controlling interests

- the effect of retrospective application or restatement for each component of equity (if applicable)

- those resulting from profit or loss

- resulting from other comprehensive income

- resulting from transactions with owners (contributions, distributions and changes in ownership)

Also, IAS 1 prescribes to present amount of dividends recognized as distributions and the related amount per share on the face of the statement of changes in equity or in the notes.

Notes to the Financial Statements

The notes are meant to be the document accompanying numerical financial statements listed above. They should provide additional information not contained in the numbers, the basis of preparation of the financial statements and some additional information that might be relevant.

IAS 1 sets that the notes shall contain a statement of compliance with IFRS , summary of significant accounting policies applied, supporting information for the numbers presented in the financial statements and other disclosures.

You can read more about the notes and how to write them in this article .

IAS 1 is shortly summarized in the following video:

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

43 Comments

Thank you for simplifying this standard . It is very helpful in my study and revision . looking forward to the other standards

A speed point machine, is it an asset that needs to be recorded in a business if they are using it?

Dear Silvia, Are prudence and conservatism concepts still applicable now under the new Conceptual Framework?

Hi I want to know can we prepare multiyear financials (i.e. 2 years to show I comparatives) as per the international auditing standards

SILIVAIA I really apprentice the presentation please can i have the ppt.?

Hi Asmera, no sorry, we only provide pdf to our subscribed students of the IFRS Kit.

Hi i have case that we debit the account Other comprehensive income (Re-measurement losses / Gain on defined benefit liability) by amount 12 Million and credit two account one of them is end of service expenses ( P&L item) by 7 Million and other account is provision of end of service by 6 Million Dr/ Other comprehensive income 12 Million Cr/ End of service expense ( P&L Item). Cr/ Provision of end of service ( Balance sheet item). my question :- 1- Other comprehensive account will be appear in balance sheet and income statement 2- and if it must appear in income statement shall we put total balance of this account 12 Million or just put 6 Million which is came from PL and ignore the 7 Million which came from provision of end of service as it is balance sheet item

This video has made my understanding of IAS 1 more clearly and understandable.I can confidently say I`am ready for the test.

I didn’t see any explanatiins for Cash Flow statement. This is also an element of Financial Statement as whole. Or would that mean it is no longer considered as part the whole reported Financial Statement?

You did not see it because it is not covered by IAS 1 (and, you are reading the article about IAS 1). You should check out IAS 7 .

Hello Silvia, Can you please help me to know as to what is the objective of creating Other Comprehensive Income and how to decide what all items should go to Other comprehensive income and Profit or loss account ?

Hi Diksha, I think this article can give you the answer . S.

hello siliva, help me with tax expense computation when u have provision, some balance due

In my opinion the documents that you share through social media is more attractive and brief to understand. I would like to follow you! Please, would you like to share brief notes and explanation on IFRS 9. By focusing MFI in detail!

Til now, I don’t understand what is the main consideration, if any, the IASB classifies a transaction as profit or loss while another as other comprehensive income. Is there any theoretical foundation or something behind the existence of other comprehensive income items?

Dear Siklus, I think this article might help . S.

Dear Sylvia, if a Company made a decision to decrease share capital (due to accumulated loss that existed on December 31, 2016) on January 17, should this be treated as an adjusting event?

Thank you very much for your help!

It depends on when the decision was made. If after 31 Dec 2016, then no, it’s non-adjusting event. S.

amazing presentation of statement of financial position but other comprehensive income should elaborate clearly. Over all presentation was very good . I also learn from that.thank you very much

Very lucid explanations. Thanks

The presentation is very knowledgeable. Is it possible for you to mail me the ppt. It would be of great help.

Hi Silvia, is it required by the standard to present the subscribed share capital with the outstanding balance of subscription receivables or a presentation of share capital would be fine?

comprehensive and material indeed

helped me tounderstand the IFRS

dear waseem…we record purchase cost as 110000.coz we did not avail the discout optiom given by the seller.

I have doubt in IAS 2. Lets say for a example, a manufacturer purchased raw material by giving 4 months pd cheque for 110,000. If they had paid by cash, price would be 100,000. What is treatment for this difference? Can we record this difference of 10,000 as finance charges?

Hey Silvia, I was about to subscribe. But I found that the name of my country (Bangladesh) is not in the list. Please let me know.

thank you for help

wow, made my studies simpler and to make sense…a superb summary indeed.

clearly and comprehensive IAS1 elaborated

Great site and well summarized IASs

very well summarized and it is very good for accounting students. thank you.

Verry good!IAS 1 !

very good indeed.impressed for days

great work………..

Great Vedio…

IT IS WELL ARRANGED OF STATEMENT.

Excellent summarized information of IAS-1

Leave a Reply Cancel reply

Recent Comments

- Kevin on Current or Non-Current?

- Antonio on Tax Reconciliation under IAS 12 + Example

- Kwen on IFRS 18 Presentation and Disclosure in Financial Statements: summary

- Yasaswi Gomes on How to account for financial guarantees under IFRS 9?

- Piper Cheng on Example: Cash flow projections and value in use under IAS 36

- Accounting Policies and Estimates (14)

- Consolidation and Groups (24)

- Current Assets (21)

- Financial Instruments (55)

- Financial Statements (50)

- Foreign Currency (9)

- IFRS Videos (68)

- Insurance (3)

- Most popular (6)

- Non-current Assets (54)

- Other Topics (15)

- Provisions and Other Liabilities (44)

- Revenue Recognition (26)

JOIN OUR FREE NEWSLETTER

report “Top 7 IFRS Mistakes” + free IFRS mini-course

1514305265169 -->

We use cookies to offer useful features and measure performance to improve your experience. By clicking "Accept" you agree to the categories of cookies you have selected. You can find further information here .

- Conceptual Framework

- IFRS Accounting Standards

IAS Standards

- IFRIC Interpretations

IAS 1 Presentation of Financial Statements

Learn the key accounting principles to be applied to financial statements, including fair presentation and compliance with IFRS Standards.

- Terms of use

- Deloitte Accounting Research Tool

© 2024 For information, contact Deloitte Global.

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms, and their related entities (collectively, the “Deloitte organization”). DTTL (also referred to as “Deloitte Global”) and each of its member firms and related entities are legally separate and independent entities, which cannot obligate or bind each other in respect of third parties. DTTL and each DTTL member firm and related entity is liable only for its own acts and omissions, and not those of each other. DTTL does not provide services to clients. Please see Deloitte website to learn more. Consult our content information page for more information about the content of this website.

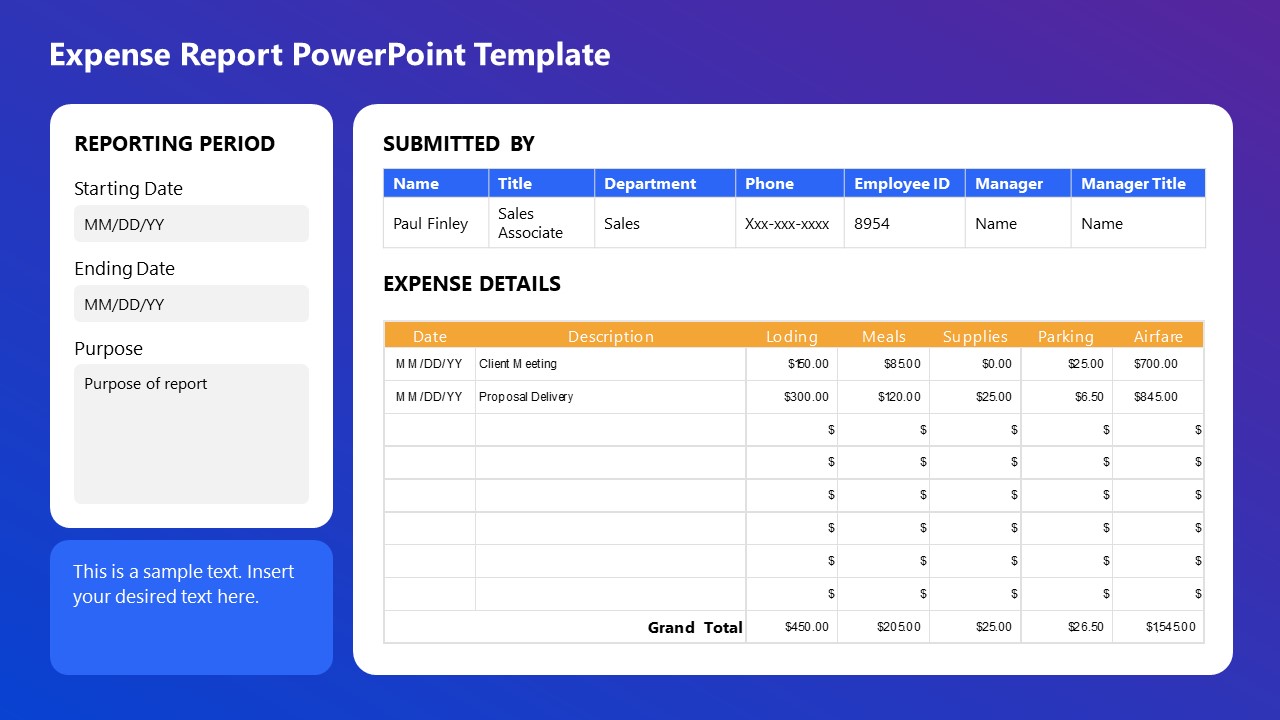

September special: Business Transformation PPT Templates

10 Slide Ideas for Financial Report Presentation

- August 17, 2021

- Financial , PowerPoint templates for download

Working on a company financial report, and want to make it different this time? Financial reviews are typically difficult to digest by non-financial audiences. It can be challenging to communicate the meaning behind the figures. If you want to disclose your quarterly or annual numbers in a simple and understandable way to your key stakeholders, check our blog for examples and inspiration.

A financial report is a management tool used to communicate key financial information to both internal and external stakeholders by covering aspects of financial affairs with the help of KPIs, such as income statements, balance sheets, cash flow, or financial ratios analysis. See how to prepare structured and professional financial slides smoothly using PowerPoint tools.

All graphics examples presented below can be downloaded as an editable source. Explore the Financial Report and Performance Indicators Presentation for PowerPoint.

Get inspired by seven examples of how you can illustrate the components of your financial report presentation and a quick instruction on how you can create a P&L Statement table using simple design tricks.

Visualize your key financial indicators

Such a general slide with a financial report presentation summary will help to analyze the big picture and ensure you’re on the same page with the audience.

You can list the common key indicators such as Global Net Revenue, Like for Like Growth, Cash Conversion Cycle, and Profit Before Tax. A neutral background picture makes the slide more attractive and circles with highlights on the right help to stay focused on important numbers.

Show revenue and profit snapshots on one dashboard slide

This slide shows how you can summarize net sales and profitability evolution using gauges and a simple bar chart. The dashboard illustrates typical profitability measures: Net Sales, Operating Expenses, EBIDTA, and PBT as easy-to-read gauge charts. The profit growth over the years is shown as a clear bar chart.

Illustrate revenue highlights with clear charts

If you’d like to include additional data, for example, revenue highlights over time or regions, you can do it as on the slides above. The first one presents a sales distribution breakdown by months and categories. The second slide example presents sales split by worldwide market geographies on a world map as a light background underlining the location of the markets.

Small elements, like pin icons, doughnut charts, and color-coding will help you add a professional look to your presentation.

Pro tip: To help non-financial people digest the data, keep your slides short, don’t stuff them with jargon words . Use illustrations, and make the most essential data points clearly visible.

Include balance sheet and cash flow tables

The very common problem is the unreadability of massive tables. The balance sheet and cash flow statement will be definitely complex, as you need to squeeze many numbers inside.

Notice how color-coding is used for various table sections, and illustrative symbols, which don’t steal attention from the content, but rather nicely add up. A text box aside can be used for your comments or notes.

Compare key drivers of revenue growth

To illustrate the comparison of several growth drivers, you can apply such stacked bars.

Notice how specific drivers (E-commerce, Emerging Markets, Organic Growth, New Product Lines) are illustrated by corresponding icon symbols, all in one consistent style.

Visualize revenue analysis for each quarter in your financial report

To present an analysis of sales revenue over the year, you can use such a bar chart. It’s slightly enhanced by adding quarter signs over the data chart.

This data chart illustrates revenue analysis split by quarters and channels. If you have some comments or notes you’d like to discuss, we advise putting the most essential point in bold.

Present your financial metrics and indicators as a dashboard grid

Want to go deeper and include the analysis of some ratios? A good idea is to firstly remind your audience what are those indicators and what exactly they show.

If you have more items to show on one slide, it’s good to organize them into some regular grid. Make sure all elements are aligned to make it look professional.

If you have more items to show on one slide, it’s good to organize them to some regular grid.

You can include general definitions and development of key financial analysis ratios e.g. growth, profitability, liquidity, efficiency, solvency, and capital market ratios. On the slide example, you can see the capital market ratios KPI line chart which shows the Dividend Yield and P/E Ratio change over the years.

Guide on how to redesign P&L Statement to a stylish table

Here’s a step-by-step guide on how you can create a P&L Statement table using simple shapes, icons, and a few tricks that will save you time.

1. Use simple PowerPoint shapes to create a stylish table design.

2. Adjust your source P&L table to be readable.

The trick is to have enough margin inside the table cell.

3. Enhance the table header

Add ribbon shapes as an additional header row to make the table look nicer.

4. Redesign the first column

You can add stylish arrows in a place of 1st table column.

5. Enrich your table with icons and a background picture.

See the whole instruction and other visual examples here: How to Create an Effective Company Financial Report Using PowerPoint.

Need to prepare a broader annual report and focus on business highlights? See how to create a comprehensive overview of activities using graphs, icons, infographic elements, and data-driven charts in this blog .

Resources: Financial Report and Performance Indicators Presentation

The graphics in this blog are a part of our financial report layouts collection. Our financial review deck incorporates 30 infographic slide templates for a financial summary overview, balance sheets with assets and liabilities, financial analysis presentation, income statements, profit and loss reports, revenue and profit snapshots, cash flow statements, explain types of financial ratios, key growth drivers, or breakdown of your operational expenses.

You can reuse graphs and charts, and tailor them to your needs in order to make your slides clear and easy to understand. See the full deck here:

Using concise, modern images will make your PowerPoint structured and consistent. To make your presentations even more appealing, consider also using this collection of professionally designed diagram layouts .

More Resources to Get Inspired

If you’re looking for more design inspiration, check our movie guide on how to present financial reports, financial analyses, and financial highlights professionally (you’ll find many more practical tips on our YouTube channel):

Subscribe to the newsletter and follow our YouTube channel to get more design tips and slide inspiration.

infoDiagram Co-founder, Visual Communication Expert

Related Posts

How to Present Machine Learning Algorithms in PowerPoint

- September 16, 2024

How to Present Inventory and Stock Metrics in PowerPoint

- August 8, 2024

Eye-catching ways to present Debtors AR report in PowerPoint

- July 31, 2024

Home Blog Business How to Make a Financial Presentation [Templates + Examples]

How to Make a Financial Presentation [Templates + Examples]

In the corporate world, many professionals excel at generating reports and financial plans, but we talk about a whole different thing regarding financial presentations. Much like report presentations , they are an entirely different discipline where overloading slides with information tends to be a common bad practice. Hence, acquiring good slide design habits from day one is important.

A financial presentation’s primary goal is to communicate a company’s financial health and performance clearly and compellingly. It goes beyond displaying numbers and charts; it requires a deep understanding of the data and the ability to weave it into a narrative that tells the story of the company’s financial journey and which is its next expected destination. In this article, you will learn how to effectively present financial results so financial professionals and stakeholders without financial education can make informed decisions based on your slides. Additionally, we will list a series of financial presentation templates to make this task easier, taking the design decisions off our hands to concentrate on content generation.

Table of Contents

What is a Financial Presentation?

What are the elements of a financial presentation, how to extract and present data from financial plans and reports, presenting financial data in visual formats, how financial presentation templates save time, recommended financial presentation ppt templates, final words.

A financial presentation is a strategic tool used within a corporate setting to convey important financial data to stakeholders. The primary purpose of these presentations is to inform decision-making processes, showcase company performance, and strategize future operations based on financial insights.

At its core, a financial presentation serves to bridge the gap between what’s understood as complex financial data and strategic business decisions . From a knowledge standpoint, it provides a framework to display financial achievements, highlight areas that need attention, and generate traction on future business decisions.

Introduction and Executive Summary

Every financial presentation should start with a clear introduction slide that outlines the objectives and what the audience can expect. This is followed by an executive summary , which offers a concise overview of the company’s financial status.

Check out our article on how to start a presentation for more ideas to break the ice at the initial stages of your financial presentation.

Financial Statements Overview

The financial statements to list are the balance sheet, income statement, and cash flow. Those three are critical; depending on the presentation’s objectives, we can add more if required. This overview is not about showing the tables but includes a brief explanation of each component, highlighting significant changes and trends that are required for the audience’s understanding.

Key Performance Indicators and Ratios

From previously defined KPIs, the presentation must list the observed changes, if the metrics meet the success criteria, and where the situation drifts from expected. Examples of KPIs are profitability, liquidity, efficiency, and leverage ratios.

If you prefer to work with the OKR approach, we invite you to check our guide on presenting objectives and key results .

Analysis of Financial Performance

After introducing all the previous data, the presenter must now examine that data, explaining trends, identifying performance drivers, and examining the variances between projected and actual numbers. The core objective is to answer why the results occurred, what they mean for the business, and which corrective measures must be implemented—if required.

Forecasting

Financial projections are presented and discussed based on current market conditions, the current financial situation, and historical data. If the data set is large enough, revenue forecasts, expenditure forecasts, and cash flow forecasts are typically displayed on individual slides. The periods to project depend on whether we are talking about an annual financial forecast, quarterly, etc.

Strategic recommendations for these future scenarios should also be included, as they give decision-makers actionable insights.

Conclusion and Call to Action

We can end the presentation with a summary of the key points discussed (especially if it was a lengthy presentation), the outlook for the company, and the core KPIs of financial health. The call to action to implement depends on the expected action to take out of the information: if making a decision, approving a strategy, or revisiting a budget, for example.

Appendices and supporting information can be delivered in handout for presentation format or include a hyperlink in the slide to access a cloud drive where all those documents can be seen.

Gathering Raw Information

The first step in preparing a financial presentation is to gather relevant data, which includes planned financials and the actual performance metrics. The planned financials refer to budget forecasts or financial targets, which are the blueprint against which actual data performance will be measured.

Data Analysis and KPIs